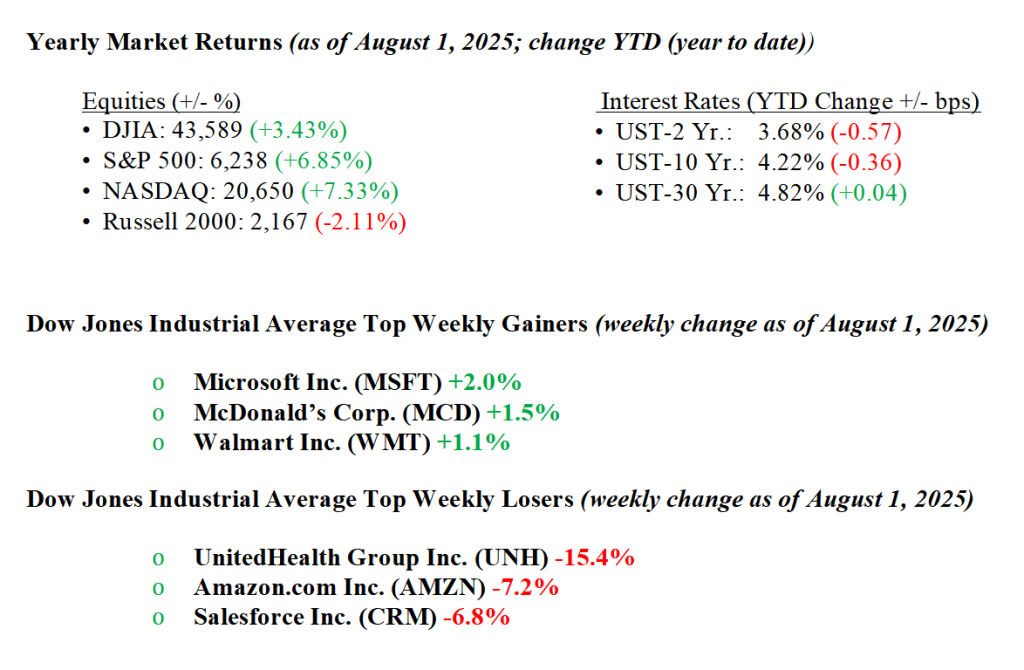

Last week, U.S. equity markets posted notable weakness, reversing the prior week’s record highs as investor sentiment soured on disappointing labor data and rising tariff concerns. The S&P 500 slid roughly 2.3%, its worst weekly decline since May, while the Nasdaq lost about 2.2%, and the Dow fell 2.9%, dragged down by renewed trade tensions. A sharply lower-than-expected July jobs report, showing just 73,000 new hires and a rise in unemployment to 4.2% after downward revisions to prior months, added to the pressure. The Federal Reserve held rates steady at 4.25–4.50%, but Chair Powell was cautious, signaling no imminent easing despite internal dissent from at least two Fed governors. Treasury yields retreated on growing odds of a rate cut; CME markets priced about a 67%–81% chance of a September move, while the 10-year note yield fell to end the week at 4.21%. Trade uncertainty intensified after President Trump announced a slate of new tariffs (10–41%) effective August 7, targeting multiple nations, exacerbating market volatility. Despite headwinds, Q2 GDP grew at an annualized 3%, and inflation measures remain somewhat elevated—core PCE at 2.8% year-over-year—adding complexity to the Fed outlook.

U.S. & Global Economy

- It was a hectic week of economic data, offering a mixed picture of the U.S. economy. Consumer confidence in July jumped to 97.2, well above expectations, and second-quarter GDP surprised to the upside with a robust 3.0% growth rate, signaling solid economic momentum. ADP private payrolls also impressed with 104,000 new jobs. Still, official labor market data painted a more troubling picture: July nonfarm payrolls came in at just 73,000, far below expectations, and job gains from the previous two months were sharply revised lower. The unemployment rate increased to 4.2%, while wage growth remained steady at 0.3% for the month. Inflation readings were firm, with core PCE holding at 2.8% year-over-year and headline PCE rising 0.3% in June. Job openings declined to 7.4 million, and pending home sales slipped by 0.8%. Despite modest personal income and spending gains, the sharp labor revisions and cooling job growth may complicate the Fed’s path forward, even amid signs of resilient overall economic activity.

Policy and Politics

- It was a busy week on the trade and tariff front, as the Trump administration rolled out significant policy changes and finalized several new trade deals ahead of the August 1 deadline. A fresh agreement with the EU set a 15% base tariff on most European goods, though steel and aluminum remain at 50%, while the EU agreed to boost investment in U.S. energy and industry. Similar deals with Japan, South Korea, Indonesia, and the Philippines helped avoid steeper tariffs, settling instead on rates between 15% and 19% in exchange for market access and investment pledges. At the same time, the U.S. raised tariffs on certain imports, including bumping Canadian goods that don’t meet USMCA standards from 25% to 35%, and slapping a 50% tariff on semi-finished copper products. India was hit with a 25% tariff plus penalties, tied to its ties with Russian oil and arms. These moves stirred fresh concerns about rising global trade tensions, with markets showing unease as businesses brace for potential retaliation and supply chain disruptions.

Economic Numbers to Watch This Week

- U.S. Factory orders for June 2025, previous 8.2%

- U.S. Trade deficit for June 2025, previous –$75.5 billion

- U.S. S&P final services PMI for July 2025, previous 52.9

- U.S. ISM services index for July 2025, previous 50.8%

- U.S. Initial jobless claims for the week of August 2, 2025, previous 218,000

- U.S. Nonfarm productivity for Q2 2025, previous –1.5%

- U.S. Unit labor costs for Q2 2025, previous 6.6%

This week presents a quieter week for economic data, but markets will still have plenty to digest thanks to a busy earnings calendar featuring several high-profile companies. Investors will get results from Palantir, Advanced Micro Devices (AMD), Caterpillar, McDonald’s, and Eli Lilly, which could influence broader market sentiment and provide insight into key sectors like tech, industrials, healthcare, and consumer services. While there are fewer major economic releases compared to recent weeks, jobless claims and trade data will still offer fresh clues about the health of the labor market and global demand. With the Fed staying on hold, attention may shift toward how corporate profits and forward guidance shape expectations for growth and monetary policy in the year’s second half. As always, at Valley National Financial Advisors, we’re watching developments closely and encourage clients to reach out with any questions about how current conditions may impact their financial plans.