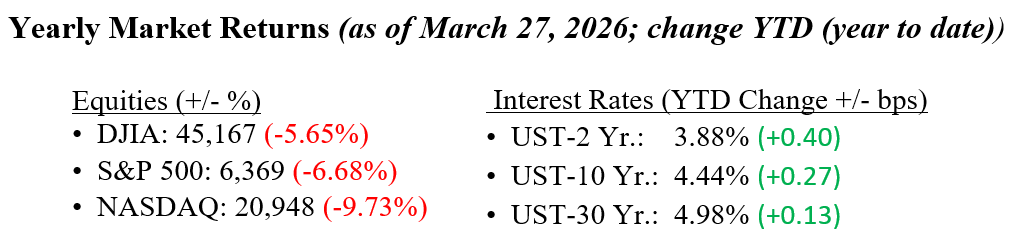

U.S. equities continued to pull back last week. The S&P 500 fell about 2.6%, the Dow Jones Industrial Average dropped roughly 2.9%, and the Nasdaq Composite declined approximately 3.1%, reflecting a continued broad-based market downturn. Markets remained under sustained pressure amid the escalation of the Iran conflict, which continues to disrupt global energy flows and has pushed oil prices firmly above $100 per barrel. This has amplified inflation concerns and further complicated the path forward for monetary policy. Treasury yields moved higher again, with the 10-year U.S. Treasury yield at 4.43%, as markets reassess the timing and magnitude of potential Fed easing. While sentiment has clearly shifted and volatility has increased amid geopolitical strain, periods like this have historically reset valuations and created opportunities. As we have stated previously in TWC, the underlying foundation of the U.S. economy remains intact. A still-resilient consumer, strong corporate balance sheets, and structural advantages such as domestic energy production should help position markets to recover as geopolitical risks retreat.

U.S. & Global Economy

- Economic data in the previous week continued to reflect a mixed but generally stable backdrop, with growing sensitivity to inflation. The most notable development was a further rise in inflation expectations, driven by sustained strength in energy prices, with oil remaining above $100 per barrel amid the ongoing Middle East conflict. On the growth side, the data continues to point to a slowing, but still positive, expansion, with no clear signs of sharp deterioration. Housing data remained uneven, with existing home sales stabilizing while new construction indicators remained volatile under the weight of higher mortgage rates. As we have noted in The Weekly Commentary, U.S. mortgage rates are largely tied to the 10-year U.S. Treasury, and amid persistent inflation concerns, fiscal imbalances, and a Federal Reserve on pause, the 10-year Treasury has remained stuck in the 4.00% to 4.50% range over the past year. The labor market continues to be a key source of resilience, with weekly jobless claims near historically low levels, signaling limited layoffs. The primary risk remains a prolonged conflict that keeps energy prices elevated, further complicating the inflation outlook and broader economic stability.

Policy and Politics

- The U.S.-Israeli conflict with Iran continued to dominate the global backdrop last week, with energy markets remaining the primary conduit for broader financial conditions. Ongoing disruptions around the Strait of Hormuz and continued strikes on regional infrastructure kept oil prices above $100 per barrel, sustaining upward pressure on inflation expectations and complicating the global policy outlook. The International Energy Agency coordinated a large strategic reserve release among its member countries, which has helped stabilize near-term supply expectations but has not fully alleviated concerns around prolonged disruption. At the same time, the Trump Administration advanced additional trade investigations, reinforcing a backdrop of rising policy uncertainty. From our perspective, while these dynamics are clearly weighing on sentiment and contributing to volatility, they remain externally driven shocks rather than a reflection of underlying economic deterioration, an important distinction as markets work through this period of adjustment. Late last week, President Trump extended the initial 5-day pause in escalation by 10 more days, providing the new Iranian regime additional time to move toward a truce rather than ongoing conflict. Sadly, international skepticism of any Iranian promise remains elevated.

Near-term market direction is likely to remain heavily influenced by the ongoing Iran conflict, oil prices, and any signs of escalation or de-escalation. Key U.S. economic releases to watch this week include the March manufacturing ISM on Wednesday and the March jobs report on Friday, which could provide insight into the resilience of the U.S. economy. Investors will also be closely watching earnings from Nike, FactSet, Restoration Hardware, MSC Industrial, and Tesla’s Q1 delivery report, as management teams are expected to provide updates on consumer and business trends since the onset of the Iran conflict. Staying focused on the long term remains critical, especially as investors have navigated similar shocks over the past few years, from the pandemic and the inflation spike to the banking crisis and Liberation Day tariff uncertainty. Your team at Valley National Financial Advisors is here to help you navigate these developments and answer any questions as conditions evolve.

Economic Numbers to Watch This Week

- U.S. Job Openings: Total Nonfarm for February 2026, prior 6.946M

- U.S. Case-Shiller Home Price Index: National for January 2026, prior $332,040

- U.S. ADP Employment Change for March 2026, prior 63,000

- U.S. Initial Claims for Unemployment Ins. for week ended March 28, 2026, prior 210K

- U.S. Labor Force Participation Rate for March 2026, prior 62.0%

- U.S. Nonfarm Payrolls, MoM for March 2026, prior -92,000

- U.S. Unemployment Rate for March 2026, prior 4.40%

Please review Important Disclosure Information set forth in the last section of this web site.