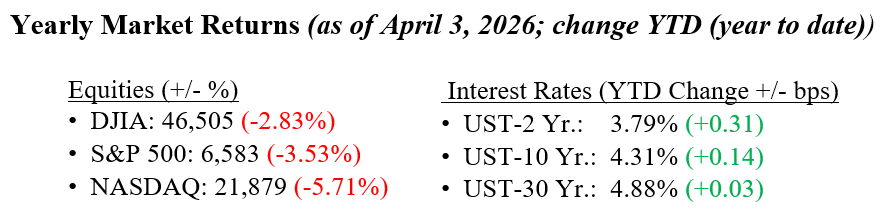

Investors began last week with a more constructive tone as signs emerged that the Iran conflict could enter a less volatile phase. Early administration messaging pointed to a potential two- to three-week window for a U.S. step-back, helping drive a strong equity rebound, with the Nasdaq Composite up 4.4%, the S&P 500 up 3.4%, and the Dow Jones Industrial Average up 3.0%. That optimism softened after President Trump’s April 1 remarks shifted the tone toward sustained military pressure, offering little clarity on when shipping through the Strait of Hormuz might normalize. Still, markets found some support in the continued two- to three-week timeframe, now viewed as a period of peak pressure rather than de-escalation. Meanwhile, reports of Iran working with Oman on a vessel-monitoring framework, and potential transit fees, provided a partial roadmap for the gradual return of oil flows, offering some stability to markets seeking clarity on global supply. Treasury bonds rallied during the week as investors moved back to safer investments. The 10-year U.S. Treasury ended the week 13 basis points lower to close the week at 4.31%.

U.S. & Global Economy

- Economic data for the week ending April 3 reinforced a more cautious consumer backdrop, with the University of Michigan Consumer Sentiment Index holding at a subdued 54.1, near cycle lows, while one-year inflation expectations rose, driven in part by elevated energy prices tied to the Iran conflict. Inflation remains sticky, with recent import and producer price data coming in firmer than expected, complicating the Fed’s path. However, Fed Chair Powell recently signaled that the central bank would likely “look through” these energy-driven spikes as temporary supply shocks, a stance that has lowered expectations for a rate hike late last week. The labor market remains a key area of stability, as Friday’s jobs report showed a stronger-than-expected rebound in hiring, with U.S. nonfarm payrolls for March rising by 178,000 while the unemployment rate edged down to 4.3%. Still, housing continues to lag, as soft builder confidence, rising incentives, and mortgage rates near 6.5% weigh on affordability and demand. Overall, the data reflects a resilient but slowing economy, where persistent inflation and higher rates are keeping consumers cautious and limiting the prospects for a near-term housing rebound.

Policy and Politics

- The U.S.-Israeli conflict with Iran continued to dominate the global backdrop last week, with energy markets remaining the main transmission channel to broader financial conditions. Disruptions around the Strait of Hormuz and continued strikes on regional energy infrastructure kept oil prices elevated and maintained upward pressure on inflation expectations, while the IEA’s record reserve release helped stabilize near-term supply expectations without eliminating concerns about a prolonged shock. At the same time, the Trump Administration advanced additional trade probes, reinforcing a backdrop of rising policy uncertainty. In our view, these developments remain externally driven shocks rather than evidence of underlying economic deterioration, even as they continue to weigh on sentiment and contribute to market volatility. Trump also extended his deadline on Iran into April 6 to allow talks to continue, though skepticism about any Iranian commitment remains elevated.

Stepping back, last week was a clear reminder of how quickly markets can shift when uncertainty begins to clear, even modestly. Strong rebounds like this often occur when sentiment is still fragile, and they are easy to miss for investors attempting to time entry and exit points. Missing just a handful of these upside movements can have a meaningful impact on long-term results. While volatility tied to geopolitical events is likely to persist, periods like this tend to reset expectations rather than alter long-term fundamentals. The underlying foundation of the U.S. economy remains intact, and staying invested, aligned with a disciplined, long-term plan, is what allows investors to participate in these recoveries rather than react to short-term noise. Your team at Valley National Financial Advisors is here to help you navigate these developments and answer any questions as conditions evolve.

Economic Numbers to Watch This Week

- U.S. ISM Services Index for March 2026, prior 56.1%

- U.S. Durable-Goods Orders for February 2026, prior 0.0%

- U.S. Personal Income for February 2026, prior 0.4%

- U.S. Personal Spending for February 2026, prior 0.4%

- U.S. PCE Price Index for February 2026, prior 0.3%

- U.S. Core PCE Price Index for February 2026, prior 0.4%

- U.S. GDP (Second Revision) for Q4 2025, prior 0.7%

- U.S. Initial Claims for Unemployment Insurance week of April 4, 2026, prior 202,000

- U.S. Consumer Price Index for March 2026, prior 0.3%

- U.S. Core Consumer Price Index for March 2026, prior 0.2%

- U.S. Factory Orders for February 2026, prior 0.1%

- U.S. Consumer Sentiment (Preliminary) for April 2026, prior 55.5

Please review Important Disclosure Information set forth in the last section of this web site.