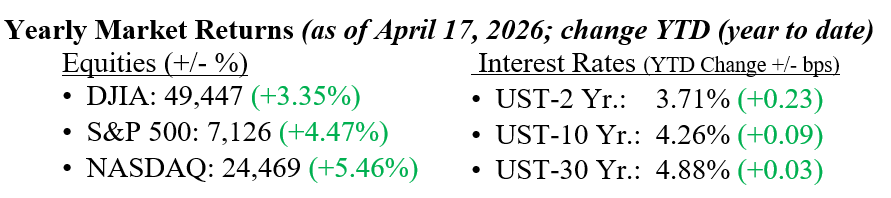

U.S. stock indexes rose 3–7% last week, marking a notable gain. While we maintain confidence in strong long-term fundamentals, last week’s jump was driven by global political shifts. Even as we write, events are rapidly unfolding. Currently, shipping through the Strait of Hormuz is “highly disrupted.” That turmoil in one region can so easily unsettle financial markets, highlighting current global volatility. Events now unfold so quickly that it often feels futile to report on them or make immediate portfolio decisions in response. Short-term news clouds the broader, ongoing transformation underneath. For years, countries have increased investments in strategic independence, particularly in energy, defense, and technology. Our message remains: tune out noise and focus on a long-term investment strategy. As we said last week, investors must continue to monitor the durability of the ceasefire and broader geopolitical risks. Last week’s treasury moves were modest, with the 10-year U.S. Treasury falling 5 basis points to close the week at 4.26%. A modest move in safe investments suggests a quieting of volatility, but we remain skeptical.

U.S. & Global Economy

- Geopolitical tensions tied to Iran are likely to continue influencing near-term economic data. This influence is seen primarily through energy. The expectation remains that these effects are temporary and won’t materially alter the longer-term growth path. This week’s inflation signals were mixed but generally stable. Core producer prices showed some moderation, rising just 0.1% month over month. Headline PPI moved higher to 4.0% year over year, reflecting ongoing energy and trade-related pressures. Elevated gas prices continue to create some near-term noise in headline inflation. Underlying trends, however, remain more contained.

- More broadly, the data reflects a slowing, but still healthy, economy. The housing and manufacturing sectors are experiencing relative weakness, as evidenced by existing home sales down 3.6%, softer builder confidence, and a 0.5% drop in industrial production. In contrast, the labor market demonstrates resilience, as initial claims fell to 207,000 and trends remain stable. Lower mortgage rates, now around 6.3%, could provide some support in the future. Stepping back, this is a typical uneven environment where not all sectors move in sync, but it’s not a sign of a breakdown. For investors, it is an important reminder: short-term data fluctuates, but staying invested and focused on the long-term plan is what ultimately drives outcomes.

Policy and Politics

- U.S. political developments this past week remained heavily centered on the situation with Iran, though the tone improved modestly. The previously announced two-week ceasefire largely held, and there were renewed signals of a reopening of transit through the Strait of Hormuz, helping ease immediate market concerns about energy supply disruptions. Diplomatic efforts continued, though progress toward a more permanent resolution remains limited and somewhat fluid. On the domestic side, the broader political backdrop remains unsettled. The partial government shutdown continues, with funding for the Department of Homeland Security still unresolved despite prior legislative efforts, and debate over executive war powers remains a point of tension in Washington.

- Trade policy also stayed front and center. The administration raised tariffs on steel, aluminum, and copper imports from specific countries to 50%. It kept a broader 10% global tariff on these metals, which remains under legal challenge. There were renewed warnings about possible tariffs targeting countries perceived to support Iran, though details about affected countries and products remain unclear. Geopolitical and policy risks remain elevated, but the market’s reaction this week suggests investors are focusing on incremental de-escalation rather than worst-case outcomes. Headlines can shift quickly; maintain a steady, long-term perspective.

The week ahead looks relatively light on economic data, shifting investor attention toward a busy slate of corporate earnings reports from major names including GE Aerospace, Tesla, IBM, Boeing, Intel, and American Express. Markets will also be watching closely to see whether the Iran ceasefire holds, as its stability could help keep downward pressure on oil prices. At the same time, interest rates remain a central theme, with ongoing debate about when the Federal Reserve may begin cutting rates. Despite these moving pieces, it’s important to look past short-term noise and remain focused on the longer-term trend of double-digit earnings growth for the S&P 500, which remains firmly intact. Your team at Valley National Financial Advisors is here to help you navigate these developments and answer any questions as conditions evolve.

Economic Numbers to Watch This Week

- U.S. Retail Sales for March 2026, prior 0.6%

- U.S. Retail Sales (Ex-Autos) for March 2026, prior 0.5%

- U.S. Business Inventories for February 2026, prior -0.1%

- U.S. Pending Home Sales for March 2026, prior 1.8%

- U.S. Initial Jobless Claims for week of April 18, 2026, prior 207,000

- U.S. S&P Flash Services PMI for April 2026, prior 49.8

- U.S. S&P Flash Manufacturing PMI for April 2026, prior 52.3

- U.S. Consumer Sentiment (Final) for April 2026, prior 47.6

Please review Important Disclosure Information set forth in the last section of this web site.