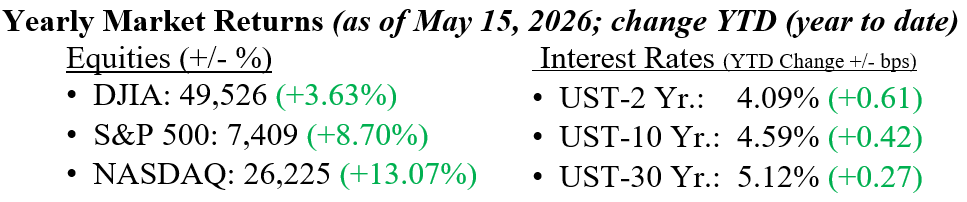

Equity markets remained resilient last week despite higher interest rates, elevated oil prices, and ongoing geopolitical uncertainty. The S&P 500 finished modestly higher, extending its winning streak to seven weeks, while the Nasdaq briefly hit a new record before retreating as Treasury yields rose. Technology and AI-related stocks continued to lead, though gains broadened somewhat into energy and defensive sectors amid renewed inflation concerns tied to oil and the Iran conflict. Sentiment stayed broadly constructive, supported by strong earnings, AI-driven capital spending, and a still-solid U.S. economy. However, volatility rose on Friday as the 10-year Treasury yield approached 4.6%, its highest level in nearly a year, while Brent crude neared $110 on concerns around the Strait of Hormuz and limited progress from the Trump-Xi summit. Despite these pressures, markets continue to absorb headline risk while maintaining a constructive longer-term trend. Markets continue to power through the noise, especially geopolitical uncertainty. As we have stated many times, the economy continues to surprise to the upside, and the U.S. Consumer remains a powerful force behind strong economic growth.

U.S. & Global Economy

- Last week’s economic data reinforced the view that the U.S. economy remains resilient, though inflation pressures have clearly reaccelerated. April CPI rose 3.8% year over year, while producer prices increased 6.0%, raising concerns that higher energy prices and tariffs may continue filtering through the economy. The labor market remained healthy, with jobless claims still signaling limited deterioration, while business investment stayed strong, particularly in AI infrastructure and technology spending. Consumer sentiment remained weak, with higher gasoline prices, inflation concerns, and geopolitical uncertainty weighing on confidence. This gap between soft sentiment and solid fundamentals remains important for investors. While inflation and higher rates may drive volatility, the economy and corporate earnings backdrop continue to support risk assets.

Policy and Politics

- U.S. policy and geopolitical developments remained a key focus for investors last week. President Trump’s summit with Chinese President Xi Jinping in Beijing covered trade, export controls, Taiwan, energy markets, and the Iran conflict. Although both sides described the meetings as constructive, few concrete agreements were announced, leaving markets somewhat disappointed. Also, nothing was resolved regarding China’s desire to absorb Taiwan, as both leaders danced around the issue rather than address it. Investors also watched the Middle East closely, especially risks around the Strait of Hormuz and global energy supplies, as oil prices rose sharply. Trade policy remained in focus as the administration pursued additional tariff measures. Despite these uncertainties, markets continue to look through headline risk, supported by earnings growth, AI investment, and broader economic strength. Maintaining discipline and long-term focus remains more important than reacting to short-term geopolitical noise.

We expect investor focus to shift from Q1 earnings toward inflation, interest rates, and the durability of economic growth. Earnings results have again been stronger than expected, supported by AI-related spending, resilient consumer demand, and healthy margins. That said, significant uncertainty remains regarding when and how the conflict with Iran will ultimately be resolved. We are closely monitoring for any signs of a pullback in consumer and business spending plans due to higher interest rates and energy prices. Although volatility may continue, the backdrop of economic resilience, healthy earnings, and continued innovation remains supportive for long-term investors. We are hopeful that market leadership will broaden beyond the large-cap AI and technology stocks that have driven much of the recent rally. Please contact your partners at Valley National Financial Advisors with any questions.

Economic Numbers to Watch This Week

- U.S. Pending Home Sales for April 2026, prior 1.5%

- U.S. Initial Jobless Claims for May 16, 2026, prior 211,000

- U.S. Housing Starts for April 2026, prior 1.50 million

- U.S. Building Permits for April 2026, prior 1.37 million

- U.S. Philadelphia Fed Manufacturing Survey for May 2026, prior 26.7

- U.S. S&P Flash Services PMI for May 2026, prior 51.0

- U.S. S&P Flash Manufacturing PMI for May 2026, prior 54.5

- U.S. Consumer Sentiment (Final) for May 2026, prior 48.2

- U.S. Leading Economic Indicators for April 2026, prior -0.6%

Please review Important Disclosure Information set forth in the last section of this web site.