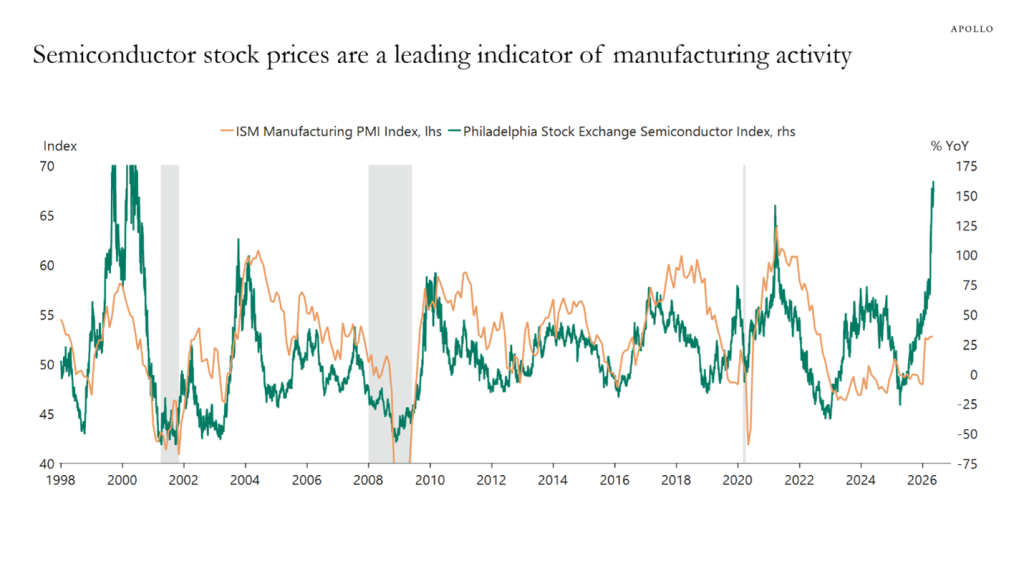

U.S. equities finished the week higher, with the Dow Jones Industrial Average gaining 2.2%, the S&P 500 up 0.9%, and the Nasdaq Composite advancing 0.5%. Investor sentiment was supported by continued enthusiasm around artificial intelligence (AI)-related stocks, helped in part by stronger-than-expected earnings from NVIDIA, which helped offset ongoing uncertainty tied to the Middle East conflict. The chart below (from Apollo) reinforces an important theme we continue to monitor closely: semiconductor stocks have historically served as leading indicators of manufacturing activity. Because chips are embedded in nearly every major manufactured product, from automobiles and industrial equipment to appliances and smartphones, rising semiconductor demand often signals strong production activity ahead. The recent surge in the Philadelphia Semiconductor Index suggests that manufacturing and capital spending trends may continue to improve over the coming quarters, reinforcing our constructive long-term outlook despite persistent headline noise surrounding inflation, interest rates, and global conflicts. The benchmark 10-year U.S. Treasury yield rose from around 4.6% at the end of the prior week to a midweek high of 4.69%, before easing back to approximately 4.56% by Friday afternoon.

U.S. & Global Economy

- Recent economic data pointed to modest but uneven growth, alongside continued inflation concerns. May’s flash PMI data from S&P Global showed overall business activity holding steady, with manufacturing activity strengthening to its highest level in four years while services activity softened slightly. At the same time, rising input costs and higher selling prices signaled persistent inflation pressures, while employment levels declined as businesses cited rising costs and weaker demand. Consumer sentiment also weakened further, with the University of Michigan Consumer Sentiment Index falling to a record low of 44.8 as households continued to feel pressure from higher living costs and rising inflation expectations. In housing, activity remained subdued as elevated mortgage rates and broader economic uncertainty weighed on demand. Builder confidence improved modestly but remained below neutral levels, pending home sales rose slightly, and housing starts declined, while the average 30-year mortgage rate climbed to 6.51%, its highest level since August. Meanwhile, labor market conditions remained relatively stable, with initial jobless claims coming in slightly better than expected at 209,000.

Policy and Politics

- The U.S. and Iran appear to be moving closer to a deal aimed at easing tensions in the Middle East, with reports indicating both sides have agreed in principle to reopen the Strait of Hormuz. However, several key issues remain unresolved, including Iran’s resistance to handing over enriched uranium and its push for immediate sanctions relief. President Trump said he is seeking a broader, long-term agreement but noted that current restrictions and the blockade would remain in place until a final deal is formally approved and signed, with final approval from Iran’s Supreme Leader still expected to take several more days. Elsewhere, the Russia-Ukraine conflict saw a modest shift over the past month, with Russian forces losing some territory after making only limited gains earlier in the year, though Russia still maintains a net territorial gain over the past 12 months. In Cuba, the Trump administration significantly expanded U.S. sanctions authority earlier this month, allowing the U.S. to target not only Cuban entities but also foreign individuals and companies involved in business activity tied to the island, marking a much broader approach similar to the sanctions frameworks used against Iran and Russia. Domestically, Kevin Warsh was sworn in as the new Fed Chair, while Fed Governor Christopher Waller struck a more cautious tone on potential interest rate cuts, contributing to higher short-term Treasury yields.

With U.S. markets closed Monday for Memorial Day, investors head into a busy week filled with earnings reports and economic data. Although earnings season is largely winding down, markets will still be paying close attention to results from AutoZone, Salesforce, Dell Technologies, and Costco. Investors will be listening closely for updates on the health of the consumer, overall business spending trends, and whether companies continue to increase investment in artificial intelligence and technology infrastructure. On the economic side, several important reports later in the week, including durable goods orders, revised first-quarter GDP data, and the Fed’s preferred inflation measure, could play an important role in shaping expectations for interest rates and the direction of the economy. Markets are also expected to remain highly sensitive to developments in the Middle East, as ongoing tensions involving Iran continue to influence oil prices and broader investor sentiment. Please contact your partners at Valley National Financial Advisors with any questions.

Economic Numbers to Watch This Week

- U.S. S&P Case-Shiller Home Price Index (20 Cities) for March 2026, prior 0.9%

- U.S. Consumer Confidence for May 2026, prior 92.8

- U.S. Initial Jobless Claims for May 23, 2026, prior 209,000

- U.S. Durable Goods Orders for April 2026, prior 0.8%

- U.S. Durable Goods Orders ex-Transportation for April 2026, prior 0.9%

- U.S. New Home Sales for April 2026, prior 682,000

- U.S. GDP (Second Revision) for Q1 2026, prior 2.0%

- U.S. Personal Income for April 2026, prior 0.6%

- U.S. Personal Spending for April 2026, prior 0.9%

- U.S. PCE Index for April 2026, prior 0.7%

- U.S. Core PCE Index for April 2026, prior 0.3%

Please review Important Disclosure Information set forth in the last section of this web site.