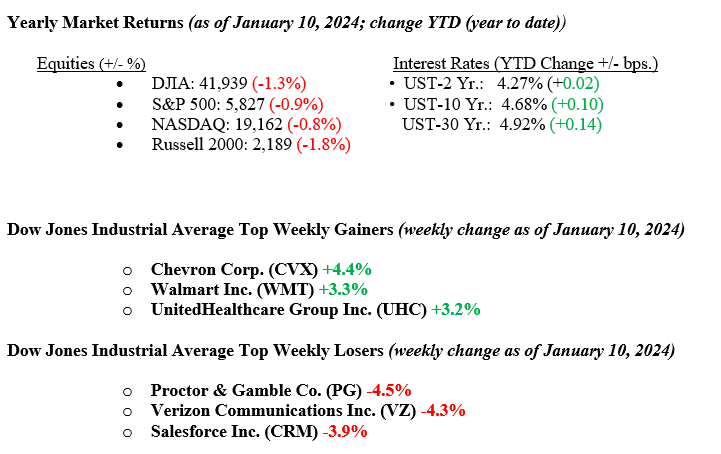

The stock market sold off last week oddly due to a positive jobs report that showed hiring was more substantial in December than economists had predicted. This paradoxical movement of stock prices falling while the economy is expanding is typical of markets during periods of uncertainty. Today’s uncertainty is “what does the Fed do in 2025?” Markets are re-pricing Fed Funds Rate cuts for 2025. Lingering inflation in the services sector and a rocket-fueled economy say rates must stay higher for longer rather than an aggressive rate-cutting strategy that economists and investors had predicted. Fixed-income markets continue to price in the two-fold reality of continuing deficits from fiscal policy and fewer rate cuts in 2025 than investors had expected just a few months ago. As a result, the yield on the 10-year U.S. Treasury bond rose 10 basis points to close the week at 4.68%. Our thesis remains that a healthy economy, a resilient labor market, and an employed and spending consumer will, in the end, better determine the direction of equity prices versus Fed rate cuts.

U.S. & Global Economy

Last week’s economic data painted an overall picture of strength in the U.S. economy despite some signs of moderation. The S&P final U.S. services PMI for December came in at 56.8, indicating solid service sector expansion, though slightly lower than expected. Similarly, the ISM Services index for December rose to 54.1%, reinforcing resilience in the sector. However, factory orders for November declined by 0.4%, signaling potential cooling in manufacturing activity. Job openings also remained elevated at 8.1 million, suggesting sustained worker demand. On the labor front, December’s ADP employment report showed a slower pace of job growth, with only 122k jobs added, below expectations, while weekly jobless claims fell to 201k, signaling a still-tight labor market. The highlight of the week came on Friday with the U.S. employment report, which revealed a stronger-than-expected gain of 256k jobs in December and a drop in the unemployment rate to 4.1%. While the jobs data underscores the economy’s resilience, these mixed signals—strong labor markets amid slowing manufacturing and moderating job growth—raised questions about whether inflationary pressures could persist, potentially influencing the Federal Reserve’s policy decisions in the coming months.

Policy and Politics

Last week, several key political developments unfolded in Washington as the country prepares for President-elect Trump’s second term. Mike Johnson (R-LA) held on to his position as Speaker of the House after receiving Trump’s endorsement, which helped win over Republican holdouts, reinforcing Johnson’s leadership and showcasing Trump’s continued influence within the party. Trump’s Cabinet nominations are set to face Senate confirmation hearings soon, with some, like Tulsi Gabbard for Director of National Intelligence, expected to face significant opposition. Reports suggest the administration is preparing nearly 100 executive orders to implement policy changes swiftly. On January 6, 2025, Vice President Kamala Harris oversaw Congress as it certified Trump’s re-election. Early signals indicate the administration will focus on immigration, border security, and tax policy, with discussions about using budget reconciliation to push these priorities forward. Trump has also commented about U.S. relations with allies, from Denmark to Panama, suggesting a potential shift in foreign policy.

Economic Numbers to Watch This Week

- U.S. NFIB (small business) Optimism Index for Dec 2024, prior reading 101.7

- U.S. Retail sales for Dec 2024, prior rate 0.4%

- U.S. Core Producer Price Index YoY for Dec 2024, prior rate 3.45%

- U.S. Producer Price Index YoY for Dec 2024, prior rate 2.98%

- U.S. Consumer Price Index YoY for Dec 2024, prior rate 2.75%

- U.S. Core Consumer Price Index YoY for Dec 2024, prior rate 3.30%

The week ahead will be busy, with numerous economic data releases and key earnings reports set to shape market expectations. On the economic front, investors will be closely watching the Consumer Price Index (CPI), Producer Price Index (PPI), Retail Sales, and the NFIB Optimism Index for insights into inflation, consumer spending, and business sentiment. The CPI and PPI reports will be crucial, as they could provide clues about whether inflation is showing signs of reigniting, potentially influencing future Federal Reserve policy decisions. These reports will offer a clearer picture of the economy’s health as we move deeper into 2025. In addition, earnings season will kick into full gear, with reports from several large-cap companies, including Wells Fargo, Citigroup, JP Morgan, Bank of America, Morgan Stanley, and Taiwan Semiconductor. These earnings updates will likely attract significant attention, offering insights into the financial sector’s performance and broader economic trends. If you have any questions or need further insights, please get in touch with your advisor at Valley National Financial Advisors.