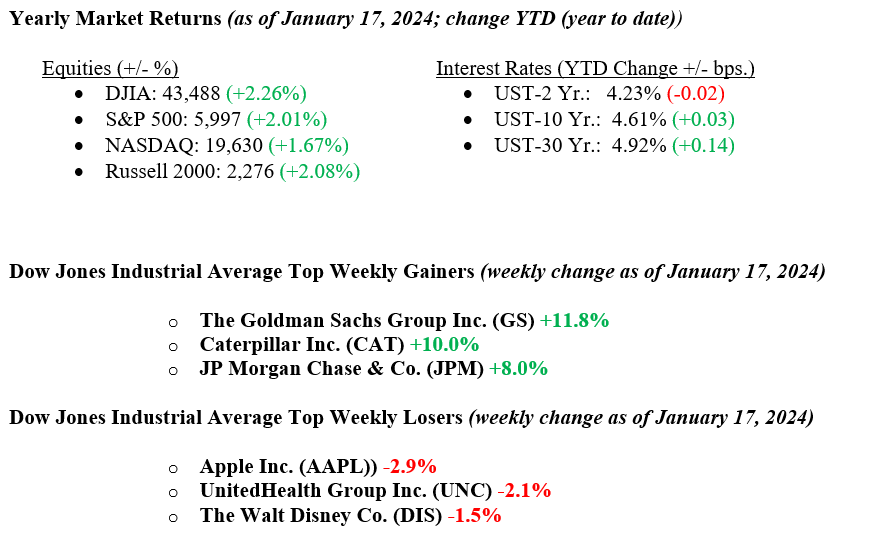

Last week, major stock indices posted substantial gains, with the Dow Jones rising 3.7%, the NASDAQ up 2.4%, and the S&P 500 gaining 2.9%. Energy was the top-performing sector, jumping 6.2%, while healthcare lagged with a modest 0.4% increase. Positive inflation data from the CPI and PPI reports provided welcome relief, helping to lower bond yields. By week’s end, the 10-year U.S. Treasury bond yield stood at 4.61%, marking a 16-basis-point decrease from the prior week. Strong earnings results from major financial institutions such as JP Morgan, Wells Fargo, Citigroup, and Goldman Sachs bolstered market sentiment. These banks provided healthy outlooks for the quarter and year ahead, further fueling investor optimism.

U.S. & Global Economy

A series of economic data points last week provided a positive view of the overall macroeconomic landscape. The NFIB optimism index for December came in stronger than expected at 105.1, signaling continued confidence among small businesses. Inflation readings showed moderation, with the Producer Price Index (PPI) for December rising 0.2%, below expectations of 0.4%, and the Core PPI increasing just 0.1%, which aligned with forecasts. The Consumer Price Index (CPI) showed a slight uptick of 0.4%, but the Core CPI rose only 0.2%, both figures still suggesting a manageable inflation environment. Jobless claims were slightly higher than expected at 217k, though still indicative of a healthy labor market. December retail sales grew by 0.4%, slightly below expectations but still signaling consumer resilience. The Philly Fed manufacturing survey and the Homebuilder Confidence Index exceeded expectations, reinforcing strength in key sectors. Overall, the data continues to reflect a stable and healthy macroeconomic picture.

Policy and Politics

Last week saw significant geopolitical developments, with Israel and Hamas agreeing to a temporary ceasefire on January 19, 2025, following months of intense conflict. The ceasefire included the release of Israeli hostages and set the stage for a potential broader prisoner exchange, offering hope for de-escalation in Gaza. On January 17, Iran’s president visited Moscow to sign a comprehensive strategic partnership, further strengthening ties between the two nations. In the U.S., the TikTok ban officially took effect on January 19, as the company refused to divest from its Chinese parent company, ByteDance. However, the decision remains ongoing and could change once former President Trump takes office again. Looking ahead, the focus shifts to the World Economic Forum meeting in Davos, running from January 20-24, where global leaders will gather to discuss critical economic and political issues facing the world today.

President-elect Donald Trump will take office on Monday, January 20, 2025, with an ambitious agenda for his first few days. We expect swift and dramatic action across multiple policy areas, including immigration, energy, economic policy, and foreign policy/trade.

Economic Numbers to Watch This Week

- U.S. leading economic indicators For Dec 2024, previous reading 0.3%

- U.S. Weekly jobless claims for the week of January 18th, prior reading 217,000

- U.S. Existing home sales for Dec 2024, prior reading 4.15 million

- U.S. Consumer sentiment (final) for Jan 2024, prior reading 73.2

- U.S. S&P flash services PMI for Jan 2024, prior reading 56.8

- U.S. S&P flash manufacturing PMI for Jan 2025, prior reading 49.4

The week ahead features a holiday-shortened trading week with limited high-profile economic data releases. Earnings season continues, with key reports expected from Netflix, Charles Schwab, Johnson & Johnson, Procter & Gamble, American Express, and Verizon. The World Economic Forum (WEF) Annual Meeting in Davos will provide a platform for interviews and insights from influential business leaders and investors. Additionally, President Trump will take office and has indicated he may sign up to 100 executive orders on his first day back in office, promising a fast-moving approach to advancing his policy agenda. Thus far, markets have reacted favorably to President Trump’s pro-growth, pro-America agenda. If you have any questions or need further insights, please get in touch with your advisor at Valley National Financial Advisors.