Last week, the equity markets showed mixed performance: the S&P 500 (-1.0%) and NASDAQ (-3.5%) both ended lower, while the Dow Jones Industrial Average saw a 1.0% gain. Tariff discussions and the collapse of the U.S.-Ukrainian mining agreement derailed a tech stock rally, prompting investors to shift toward more stable industrial and dividend-paying stocks. Furthermore, a report from the U.S. Conference Board showed a drop in consumer confidence in February by 7 points to 98.3. Details from the report showed that survey participants had fresh concerns about inflation. Friday’s Personal Consumption Expenditures Index report showed that inflation continues to be at levels above the Fed’s long-term target of 2.0%. As is typical of the stock market, uncertainty creates volatility and a general flight to quality, which we saw last week with U.S. Treasury bonds rallying. The 10-year U.S. Treasury bond yield ended at 4.29%, twenty-three basis points lower than the previous week.

U.S. & Global Economy

While there has been some slowing in economic activity, economists are calling for a healthy 2.3% growth in GDP for 2025. An aggressive tariff strategy could further harm economic growth, but ‘uncertain’ is perhaps the most fitting description of the tariff policy coming from the White House. The U.S. has been adding an average of 230,000 new jobs each month over the past three months, and consumer spending continues to be aided by a steady growth in wages. Lastly, we expect AI-related tools and solutions to begin benefiting a broader range of businesses across the economy, moving beyond just the small group of companies building the chips and infrastructure that enable AI adoption.

Policy and Politics

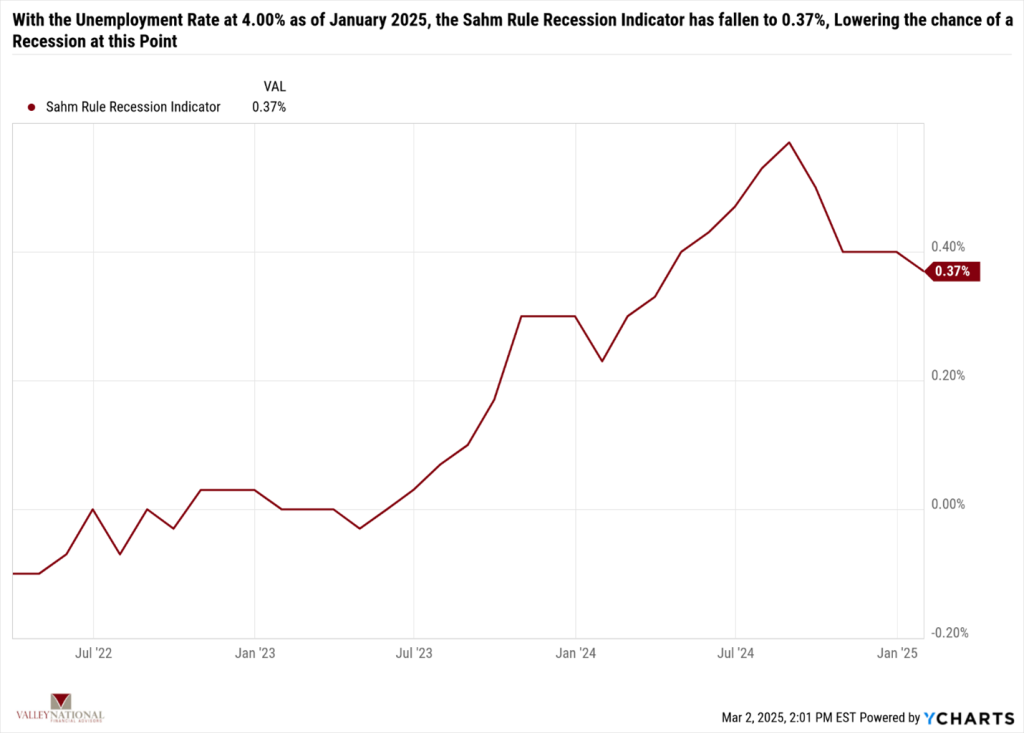

Last week, President Trump indicated that tariffs on Canada and Mexico would start on March 4, paired with an extra 10% levy on Chinese imports. This on-again / off-again trade policy uncertainty is beginning to impact consumer confidence and, therefore, growth prospects for the U.S. economy. Despite this, the probability of a recession remains low, and the Sahm Rule, a noteworthy predictor of recessions, has fallen for three straight months. See Chart 1 below from Valley National Financial Advisors and Y Charts showing the Sahm Rule.

Lastly, an article last week in Bloomberg discussed a $1 trillion pledge by U.S. tech giants to invest in ventures inside the United States. Companies such as Apple, OpenAI, Meta, Softbank, and Amazon were all mentioned in the article as being part of the pledge. While President Trump will take credit for the pledge, the impact is the same regardless of the source. We view this as bullish for both the U.S. economy and our financial markets.

Economic Numbers to Watch This Week

- U.S. ISM manufacturing for February 2025, prior level, 50.9%

- U.S. ISM Services for February 2025, prior level, 52.8%

- U.S. Factory Orders for January 2025, prior level, -0.90%

- U.S. Initial Claims for Unemployment Insurance for the week of March 1, 2025, prior 242,000

- U.S. Labor Force Participation Rate for February 2025, prior rate 62.60%

- U.S. Nonfarm Payrolls MoM for February 2025, prior level 143,000

- U.S. Unemployment Rate for February 2025, prior level 4.0%

This week, earnings reports from major consumer companies like Costco, Target, Kroger, and AutoZone will provide valuable insights into the condition of the U.S. consumer, especially considering the recent softening in consumer confidence. Investors will also be paying close attention to the February employment report for signs of any weakness in the jobs market following recent government job cuts. We believe the U.S. economy remains on solid footing, buoyed by low unemployment, solid consumer and bank balance sheets, and a healthy housing market. Although tariffs and geopolitical tensions may create short-term uncertainty and volatility, we remain focused and optimistic about the long-term outlook. If you have any questions or need more information, feel free to reach out to your advisor at Valley National Financial Advisors.