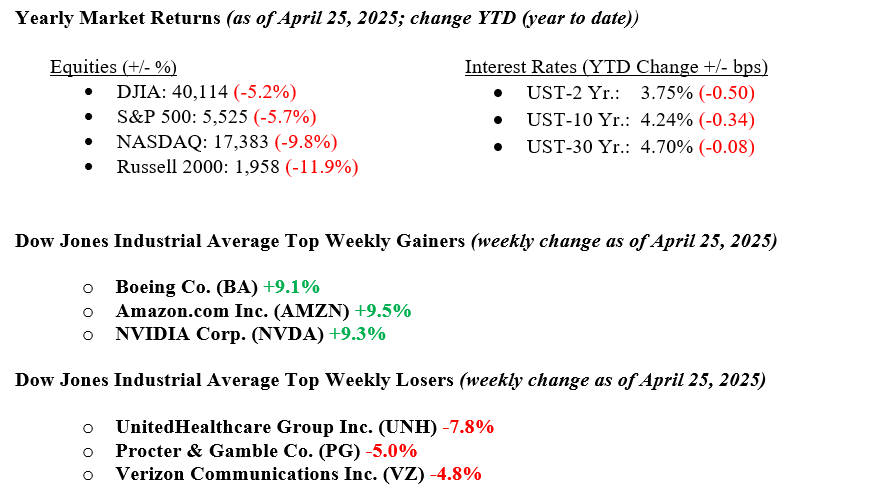

U.S. stock markets rallied last week, recovering from tariff-driven volatility from earlier in the month. The Dow Jones Industrial Average rose 2.5%. The S&P 500 gained 4.6%, its strongest weekly performance since October 2023. The Nasdaq Composite surged 6.7%, propelled by strong technology sector gains. The Russell 2000 advanced 4.0%. Investor optimism was fueled by Treasury Secretary Bessent’s remarks that U.S.-China tariffs were unsustainable, raising hopes for trade negotiations, though President Trump’s late-week tariff threats tempered gains. The technology and communication services sectors, led by Tesla and Nvidia, outperformed, while healthcare and utilities lagged. The CBOE Volatility Index (VIX) futures fell 15%, signaling reduced market fear. The U.S. dollar index increased 0.2%, and gold and oil prices dipped slightly amid trade optimism. Federal Reserve Chair Powell’s cautious comments on inflation and tariffs underscored ongoing policy uncertainty, while reports of China considering tariff exemptions for some U.S. goods further lifted sentiment. The 10-year U.S. Treasury yield dipped to 4.24%, down from 4.31% the prior week, reflecting calmer bond markets.

U.S. & Global Economy

Last week, U.S. economic data showed a mix of resilience and warning signs. The Leading Economic Index fell 0.7% in March, a bigger drop than expected, suggesting some slowdown ahead. Business activity was a bit of a mixed bag—services cooled off more than anticipated, with the S&P flash services PMI slipping to 51.4. At the same time, manufacturing came in a bit stronger than expected at 50.7. The housing market sent conflicting signals: new home sales jumped to 724,000, beating forecasts as builders offered more incentives. However, existing home sales dropped sharply to 4.02 million—the steepest decline since 2009—thanks to high mortgage rates and affordability challenges. Durable goods orders posted a massive 9.2% gain, driven mainly by aircraft orders, but excluding transportation, orders were flat. Jobless claims held steady at 222,000, pointing to continued strength in the labor market. Fed officials and economists took note of the mixed signals, acknowledging the strong labor data and resilient demand in some sectors but also expressing concern about slowing momentum and lingering inflation pressures. Markets continue to look for clues on when the Fed might make its next move on interest rates.

Policy and Politics

Markets were a bit uneasy last week, as geopolitical tensions and trade uncertainty took the spotlight. Peace talks over the Russia-Ukraine war hit a snag after former President Trump criticized Ukrainian President Zelensky, just as Russia launched another major missile and drone attack on Kyiv. Putin suggested the idea of direct talks with Ukraine for the first time in years, but U.S. efforts in Moscow didn’t seem to make much progress. There were even rumors that the U.S. might recognize Russia’s control of Crimea to help reach a deal, though nothing was confirmed. In the Middle East, ceasefire talks between Israel and Hamas remained stuck, despite some minor progress reported by Qatar, while airstrikes from Israel continued. On the trade front, things settled a bit between the U.S. and China after Treasury Secretary Scott Bessent mentioned that current tariffs weren’t sustainable. Markets got a brief boost from rumors that China might ease tariffs on U.S. goods, but by the end of the week, Trump threatened to impose 50% tariffs on Chinese imports, bringing uncertainty back into the picture. While Washington continues to talk about progress on trade, no solid deals have been made yet, leaving investors feeling cautious.

Economic Numbers to Watch This Week

- U.S. Consumer Confidence for April 2025, prior 92.9.

- U.S. Job Openings for March 2025, prior 7.6 million.

- U.S. ADP Employment for April 2025, prior +155k.

- U.S. GDP Q1 2025, prior 2.4%.

- U.S. Consumer Spending for March 2025, prior 0.4%.

- U.S. PCE Index for March 2025, prior 0.3%.

- U.S. Core PCE Index for March 2025, prior 0.4%.

- U.S. Initial Claims for Unemployment Insurance for the week of April 26, 2025, prior 222K.

- U.S. ISM Manufacturing for April 2025, prior 49.

- U.S. Nonfarm Payrolls for April 2025, prior +228k.

- U.S. Unemployment rate for April 2025, prior 4.2%

The week ahead is packed with major earnings reports from big names like Amazon, Apple, Meta, Microsoft, Mastercard, and Visa. Investors will be closely watching for updates on AI-related investments as companies like Microsoft, Amazon, and Meta continue to ramp up spending in this space. Visa and Mastercard will also provide insights into current consumer spending trends, helping us understand how resilient the consumer market is, especially in areas like travel and entertainment. On the economic front, we’ll get a batch of important data, including Q1 GDP, job openings, and consumer sentiment, all of which will give us a clearer picture of the overall economic landscape. Despite continued trade uncertainty, the economy is holding steady, supported by healthy corporate earnings and a solid jobs market. If you have any questions or need more information, contact your advisor at Valley National Financial Advisors.