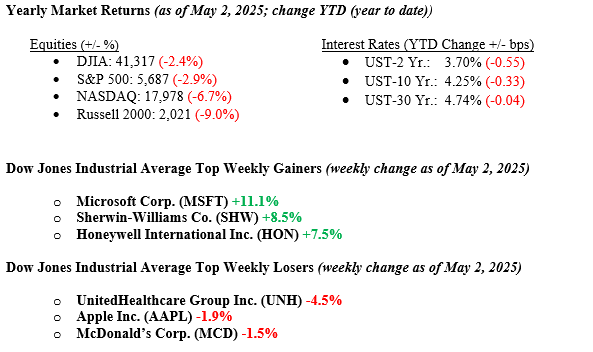

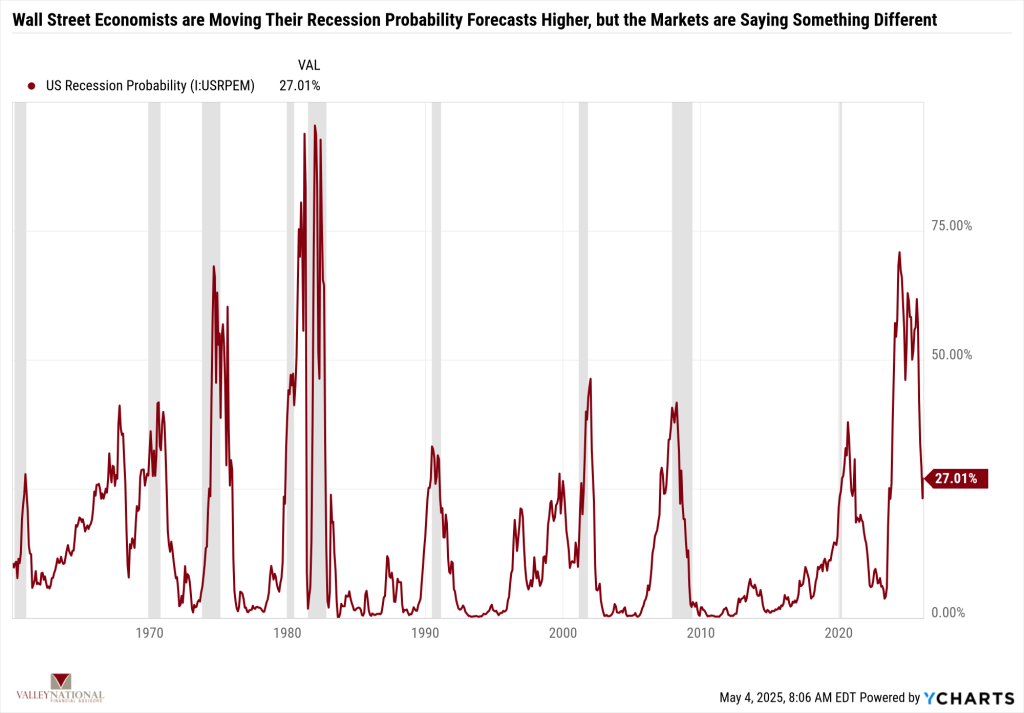

Wall Street got a dose of mixed messages last week, as a negative GDP print for Q1 2025 (-0.30%) warned of a coming recession, and an above-expectation payroll number (+177k) on Friday screamed “things are still ok” to traders and investors. Each primary stock market index increased by +3.0% for the week, marking the ninth straight positive day for U.S. equities. Strong earnings results and outlooks from Microsoft and Meta added to market optimism, with both companies highlighting continued strength in AI-related spending and deployment. Policy uncertainty remains the biggest stumbling block to a growing economy, weighing on consumer confidence. While many economists have increased their probability of recession, the markets are showing only a 27% chance (see Chart 1 below). The Federal Reserve meets this week and is widely expected to leave interest rates unchanged. The 10-year U.S. Treasury yield increased by only one basis point to 4.25%, reflecting calmer bond markets.

U.S. & Global Economy

Economic data points from last week were mixed but showed the U.S. economy remains resilient despite tariff-related uncertainty and challenges. While several indicators, including consumer confidence, job openings, and ADP employment figures, came in below expectations, the labor market remained relatively solid, with April nonfarm payrolls rising by 177,000—beating expectations—and the unemployment rate holding steady at 4.2%. The first estimate of Q1 GDP showed a surprise contraction of 0.3% versus expectations for modest growth, but this was largely due to a sharp increase in imports as businesses accelerated purchases ahead of anticipated tariffs rather than a fundamental weakness in domestic demand. Inflation remained muted, with both the PCE and core PCE indices flat for March. Manufacturing data was mixed but showed some stabilization. Overall, the economy continues to demonstrate underlying resilience in the face of trade-related disruptions and geopolitical uncertainty.

Policy and Politics

Trade and tariff talks have shown some early progress, especially between the U.S. and China, with Beijing saying it is “evaluating” U.S. proposals to start negotiations. However, China still demands that the U.S. roll back its recent tariff hikes before real talks begin. There have been informal contacts and discussions in Washington about possibly easing tariffs. Adding to speculation, U.S. Commerce Secretary Howard Lutnick said on April 29 that a trade deal with an unnamed country was done but still needed approval from that country’s prime minister and parliament. Meanwhile, the U.S. and Japan have started talks, but little progress has been made on key issues like auto and metal tariffs. Overall, there are hints of movement, but no breakthroughs yet.

In recent days, both the Russia-Ukraine and Israel-Gaza conflicts have escalated, with heavy fighting continuing and ceasefire efforts stalled. In Ukraine, Russian forces have intensified attacks despite suffering heavy losses, while Ukraine rejected a proposed short-term ceasefire as insincere. The U.S. responded with new military aid for Ukraine. In Gaza, Israel has mobilized tens of thousands of reservists to expand operations amid a deepening humanitarian crisis, stalled negotiations, and rising domestic protests. In both conflicts, limited progress has been made toward peace as violence and instability persist.

Economic Numbers to Watch This Week

- U.S. ISM Services for April 2025. Prior rate 50.8%

- Fed Funds Rate as of May 7, 2025, current rate 4.50%

- U.S. Productivity for Q1 2025, prior 1.50%

- U.S. Unit Labor Costs: Nonfarm Business QoQ for Q1 2025, prior rate 2.20%

- 30-year Mortgage Rate for the week of May 8, 2025, prior rate 6.76%

This week’s economic calendar is relatively light, focusing mainly on the upcoming Federal Reserve meeting and Chair Powell’s press conference. Markets widely expect interest rates to remain unchanged. Attention will also turn to a busy slate of corporate earnings, with key reports due from Disney, Advanced Micro Devices, Arm Holdings, Uber, and Novo Nordisk. In addition, markets will be watching closely for any updates on tariffs and trade negotiations as investors look for signs of progress or potential setbacks. While the recent equity market rebound is encouraging, we believe pressure is mounting for concrete trade deal victories as we have reached the one-month mark since the Liberation Day tariff announcements. If you have any questions or need more information, contact your advisor at Valley National Financial Advisors.