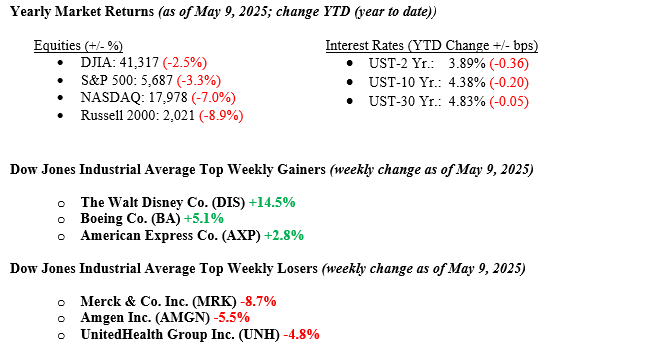

Despite a busy week of major headlines, including the Fed holding rates steady, a new U.S. and U.K. trade deal, and the historic naming of the first American Pope, markets showed little movement, and the major indexes ended the week essentially unchanged. Given the recent news of tariff agreements between the U.S. and China, the Fed’s “wait-and-see” approach to rates is the appropriate strategy. Fed Chairman Powell noted that risks remain in the economy. Still, more importantly, there is no rush to lower rates given the continued strength in the economy’s labor market and services sector. Earnings season for the first quarter has essentially wrapped up, and EPS are expected to rise 13.4%, according to FactSet. This will mark another strong earnings season as companies report very healthy results. The 10-year U.S. Treasury yield increased by 13 basis points to close the week at 4.38%. We have seen the markets rebound nicely since their April sell-off. This proves once again that patient investors are smart investors, and staying invested for the long term is always the winning strategy.

U.S. & Global Economy

As widely anticipated, the Fed held the target range for the federal funds rate at 4.25–4.50%. Both the rate decision and accompanying statement passed without incident, markedly neutral in tone and underscoring the prevailing uncertainty. The only notable nuance was the FOMC’s acknowledgment that it faces a trade-off between growth and inflation and between inflation and potential job losses. There was no update to the Summary of Economic Projections at this meeting.

Looking ahead, the outlook remains uncertain. President Trump’s tariff announcements and the ensuing retaliatory measures have unsettled markets, prompting companies to devise contingency plans and withdraw forward earnings guidance. Investors are struggling to find stable ground amid protracted trade negotiations. Meanwhile, economic activity is already cooling: the Q1 GDP report at month’s end confirmed a contraction, and both survey indicators and high-frequency data (for example, container‐ship volumes) paint a similar picture. Tariffs are dragging on growth even as they stoke price pressures, creating a delicate balancing act for the Fed, a challenge Chairman Powell briefly highlighted in his press conference. This week, we will get another reading on inflation with the Consumer Price Index, which is scheduled to be released on Tuesday.

Policy and Politics

Trade and tariff talks have shown some early progress, with the U.S. and the U.K. reaching a comprehensive trade agreement. Further, over the weekend, China and the U.S. met in Switzerland to begin a series of discussions aimed at reaching another trade agreement.

Among other Washington news, diplomats from all circles are working to arrange peace talks or ceasefires in three major conflict regions: Russia/Ukraine, India/Pakistan, and Israel/Hamas. We do not expect quick fixes to long-lived conflicts, but we are hopeful that peace is at hand for all.

Economic Numbers to Watch This Week

- U.S. NFIB (small business) optimism index for April 2025, prior reading 97.4

- U.S. Consumer Price Index for April 2025, prior rate –0.1%

- U.S. Weekly initial jobless claims for the week of May 10, 2025, prior reading 228,000

- U.S. Retail Sales for April 2025, prior rate +1.4%

- U.S. Producer Price Index for April 2025, prior rate –0.4%

- U.S. Empire State manufacturing survey for May 2025, prior reading –8.1

- U.S. Philadelphia Fed manufacturing survey for May 2025, prior reading –26.4

- U.S. Import Price Index for April 2025, prior rate –0.1%

- U.S. Consumer sentiment (prelim) for May 2025, prior reading 52.2

As earnings season winds down, results have generally exceeded expectations, possibly boosted by some preemptive consumer and business purchasing activity ahead of anticipated tariffs. While most major Q1 reports are in, the market will watch this week’s earnings from Walmart, John Deere, Applied Materials, and Cisco for any signals on tariff impacts. The economic calendar is busy with April data on small business optimism, retail sales, CPI, PPI, and consumer sentiment, which will help gauge the broader economic outlook. The UK and China trade deals are encouraging, but we remain cautious as markets have rebounded sharply despite lingering uncertainty facing businesses around Fed policy and other global tensions. We expect companies to adjust their capex plans now that the major obstacle (China/U.S.) is nearing a conclusion. If you have any questions or need more information, contact your advisor at Valley National Financial Advisors.