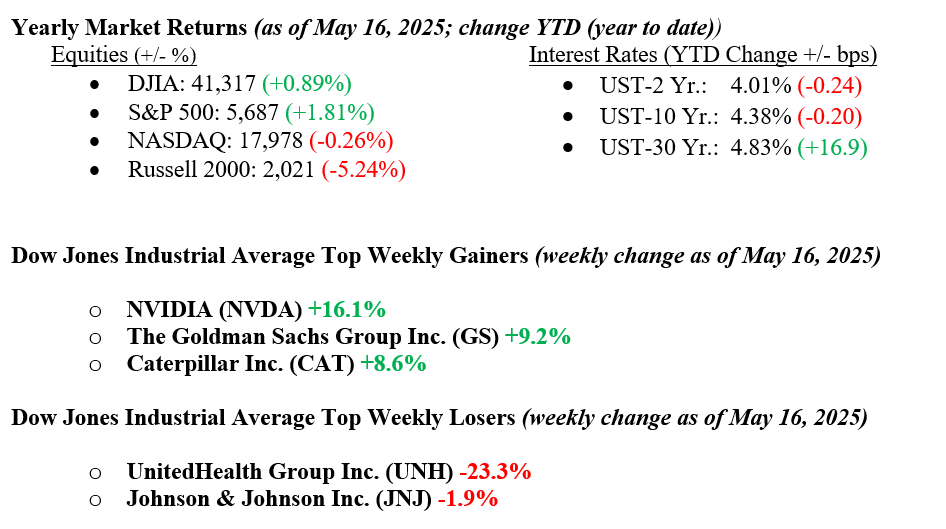

Equity markets surged last week, with the S&P 500 up 5.27%, Nasdaq 6.81%, Dow 3.41%, and Russell 2000 4.46%, as sentiment shifted from extreme fear to optimism. Several positive developments fueled the rally. Progress on U.S.-China trade talks, including a 90-day tariff pause and some reductions, helped ease tensions. Inflation also came in cooler than expected, with April CPI and PPI readings both surprising to the downside. In addition, President Trump’s Middle East tour brought encouraging headlines, including reports of a potential U.S.-Iran nuclear deal. These positive signals boosted market confidence and led investors to push out expectations for the first Fed interest rate cut from June to September. The S&P 500 closed above its 200-day moving average, a bullish technical indicator, while Goldman Sachs cut its recession odds to 35%, below the Bloomberg consensus of 40%. Crude oil rose to $61.15 (+1.24%), and the 10-year Treasury yield increased to 4.48% (+10 bps).

U.S. & Global Economy

The U.S. economy remains relatively well despite lingering trade uncertainty, with recent data showing resilience and cooling inflation. April’s CPI and Core CPI rose 0.2%, slightly below forecasts, while PPI and Core PPI unexpectedly declined by -0.5% and -0.4%, respectively, relieving inflation pressures. Retail sales were flat in April, and jobless claims remained steady at 229,000. Small business optimism increased to 95.8, manufacturing surveys improved modestly, and the Philly Fed index jumped to -4.0 from -26.4. However, homebuilder sentiment declined sharply to 34. While the recent 90-day tariff pause between the U.S. and China offers short-term relief, it may distort near-term economic data, as companies rush to act before tariffs potentially return. Trade negotiations remain fluid, with much work ahead before reaching a lasting resolution.

Policy and Politics

Last week, the U.S. and China announced a better-than-expected 90-day tariff pause following high-level talks in Geneva, significantly reducing tensions that had weighed on global markets. The U.S. agreed to lower tariffs on Chinese goods from 145% to 30%, while China cut its tariffs on U.S. goods from 125% to 10%. The deal also retains a 10% universal U.S. tariff and a 20% tariff on fentanyl-related products. It includes a framework for ongoing talks on unresolved issues like the trade imbalance and fentanyl smuggling. While the pause brought welcome relief, it stopped short of delivering breakthroughs, and many analysts noted that substantial work remains. Meanwhile, President Trump’s visit to Saudi Arabia, Qatar, and the UAE focused on expanding economic ties, including a $600 billion Saudi investment pledge in U.S. infrastructure and a $10 billion Qatari commitment to support a U.S. airbase. Talks during the trip also pointed to potential movement toward a renewed nuclear deal with Iran.

Recent developments in global conflicts include continued tension in Ukraine, where Russia and Ukraine held their first ceasefire talks in three years, though no agreement was reached. In Gaza, the death toll has surpassed 53,000 as Israeli forces maintain their offensive against Hamas. Meanwhile, in the India-Pakistan dispute, tensions remain high following India’s military operation in Pakistan-administered Kashmir, with both sides exchanging strikes, though a ceasefire was briefly agreed. India is also considering measures to restrict Pakistan’s water supply from the Indus River, which could escalate tensions further.

Economic Numbers to Watch This Week

- U.S. Leading Economic Indicators for April 2025, prior reading –0.7%

- U.S. Weekly initial jobless claims for the week of May 17, 2025, prior reading 229,000

- U.S. Manufacturing PMI for May 2025 (prelim), prior 50.2

- U.S. Services PMI for May 2025 (prelim), prior 50.8

- U.S. Existing Home Sales for April 2025, 4.02 million prior

- U.S. New Home Sales for April 2025, 724k prior

As trade discussions continue, early agreements with the U.K. and China are encouraging, though key details remain unresolved, and negotiations with other trading partners still need to advance. Despite ongoing uncertainty around tariffs, the U.S. economy continues to show resilience. The labor market remains healthy, and consumer spending is holding up well, offering a solid foundation. This week will be relatively quiet on the economic and earnings front, with few major data releases or corporate reports expected. As a result, investor focus is likely to shift toward developments in global trade negotiations and progress on the “Big Beautiful Bill”—a broad legislative package that includes tax cuts, spending reductions, and a $4 trillion increase in the debt ceiling. While recent stock market gains have been impressive, the backdrop of still high uncertainty and trade-related economic challenges suggests that volatility is likely to persist. If you have any questions or need more information, contact your advisor at Valley National Financial Advisors.