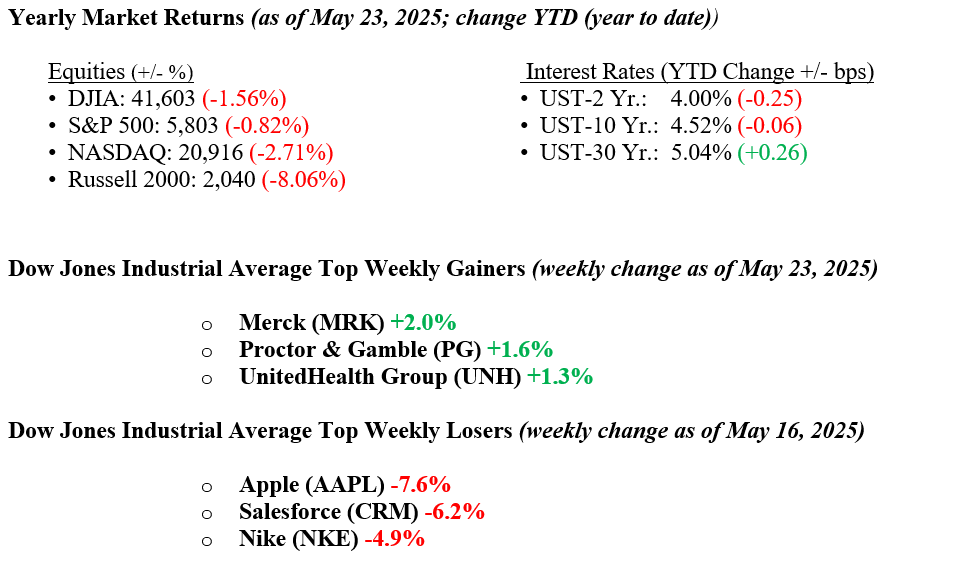

Equity markets experienced a downturn last week, with the S&P 500, Nasdaq, and Dow Jones Industrial Average declining approximately 2.5% and the Russell 2000 dropping around 3.5%. This retreat occurred amid rising U.S. Treasury yields and renewed trade tensions. Moody’s downgraded the U.S. credit rating from Aaa to Aa1 on May 16, the first downgrade in its 108-year history, citing rising federal debt, interest costs, and political dysfunction, echoing S&P’s 2011 downgrade. Trade concerns intensified as President Trump proposed a 50% tariff on European Union imports and a 25% tariff on smartphones manufactured outside the U.S., targeting companies like Apple. JPMorgan CEO Jamie Dimon warned that markets are underestimating the impact of tariffs, predicting a sharp slowdown in S&P 500 earnings growth. Housing data was weak, with existing home sales in April hitting their lowest level since the financial crisis. Meanwhile, Trump’s narrowly passed tax bill (214-215) raised concerns about a surging deficit. Despite these challenges, Amazon CEO Andy Jassy provided a glimmer of optimism, stating that the company hasn’t observed signs of consumers pulling back their spending despite the new tariffs. This positive outlook on consumer behavior offered a hopeful note amid a week dominated by negative headlines. For the week, the 10-year Treasury yield increased to 4.52% (+4 bps)

U.S. & Global Economy

Last week was relatively light on economic data, but several key indicators provided insight into the current U.S. economy. Initial jobless claims for the week ending May 17 totaled 227,000, slightly below the expected 230,000 and the previous week’s 229,000, suggesting ongoing labor market stability. The S&P Global flash Purchasing Managers’ Index (PMI) readings for May indicated expansion in the services and manufacturing sectors, with both indices at 52.3, surpassing expectations of 50.6 and 49.8, respectively. This suggests moderate growth in business activity. In the housing market, April’s existing home sales came in at 4.0 million, slightly below expectations, as activity remains stuck with many homeowners unwilling to sell due to their low mortgage rates. While the week lacked major economic announcements, these data points indicate a mixed but cautiously optimistic economic landscape. However, looking ahead, financial data may become increasingly choppy and difficult to interpret as on-and-off tariff developments continue to create uncertainty, with many companies accelerating purchases in anticipation of potential future tariffs, temporarily distorting underlying trends in demand and activity.

Policy and Politics

Last week, significant developments in U.S. trade policy shook markets and raised concerns about the economy’s outlook. On May 23, President Trump announced a sweeping 50% tariff on all European Union imports set to take effect June 1, citing stalled trade negotiations and what he labeled as systemic unfair trade practices by the EU. The announcement sent shockwaves through international markets, contributing to a 1.7% decline in the Stoxx Europe 600 index and prompting immediate criticism from European leaders, who warned of retaliatory measures. In a separate but related move, Trump threatened to impose a 25% tariff on Apple unless the company shifted iPhone component production to the U.S. This demand lowered Apple’s stock. It also raised concerns about broader supply chain disruptions in the tech sector. These aggressive trade actions came alongside the narrow passage of Trump’s signature tax bill in the House by a 214-215 vote. The bill includes a package of extended tax cuts and spending offsets that many economists say could significantly widen the federal deficit if not paired with new revenue sources. While Trump administration officials suggested increased tariff revenues could help offset the cost, critics expressed skepticism.

Economic Numbers to Watch This Week

- U.S. Durable Goods Orders for April 2025, prior +9.2%

- U.S. Consumer Confidence for May 2025, prior 86.0

- U.S. Weekly initial jobless claims for the week of May 24, 2025, prior to 227,000

- U.S. GDP (first revision) for Q1 2025, initial report –0.3%

- U.S. Personal Income for April 2025, prior 0.5%

- U.S. Consumer Spending for April 2025, prior 0.7%

- U.S. PCE Index for April 2025, prior 0.0%

- U.S. Core PCE Index for April 2025, prior 0.0%

Markets will be focused this week on a series of high-profile corporate earnings reports that could offer important insights into the health of consumer spending, enterprise demand, and AI-driven growth. NVIDIA headlines the week with much-anticipated results on Wednesday as investors look for confirmation that enthusiasm around artificial intelligence is translating into sustained revenue gains. Dell, Salesforce, and Costco will also report, providing a broader view of trends in technology, corporate IT spending, and consumer behavior. While economic data remains essential, especially amid persistent inflation and rate uncertainty, earnings from these bellwether companies may significantly shape the market direction in the near term. Last week served as a reminder that significant risks still loom around tariffs, trade disputes, and the broader push to bring manufacturing back to the U.S. We will continue to monitor developments for signs of weakening in employment or overall economic activity. If you have any questions or need additional guidance, please get in touch with your advisor at Valley National Financial Advisors.