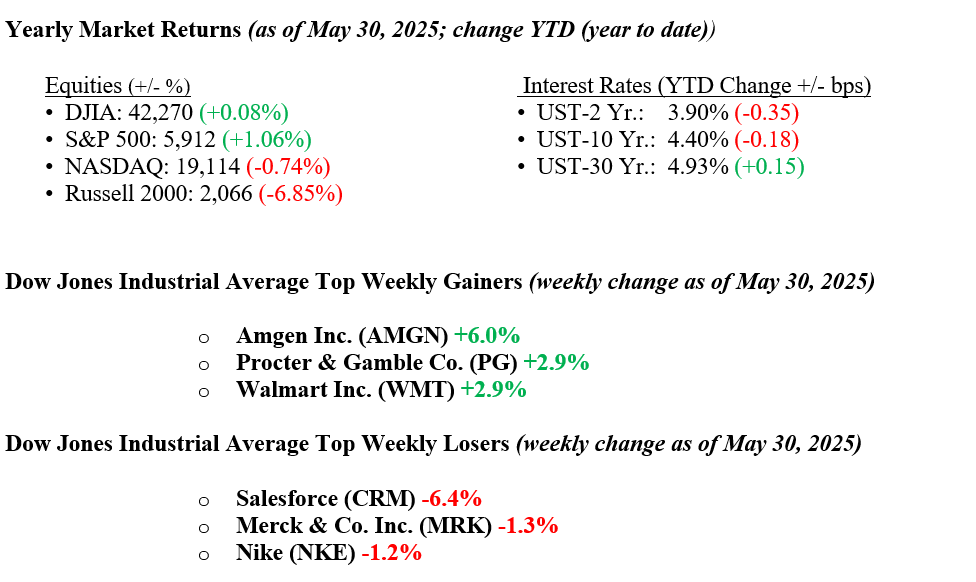

Equity markets rallied across the board last week, with each major index rising by +1.0%. A combination of positive developments helped fuel the momentum. President Trump’s decision to pause tariffs on the European Union until July 9, 2025, gave investors a temporary reprieve from trade tensions, even as the EU’s proposed 50% retaliatory tariffs were delayed to the same date. While the Federal Trade Court initially blocked Trump’s tariffs on Wednesday, an appeals court reinstated them on Thursday, keeping some uncertainty in play. Tech stocks rose midweek after AI tech bellwether, NVIDIA, reported strong earnings and issued upbeat forward guidance, adding further strength to the rally. Meanwhile, the Conference Board’s Consumer Confidence Index rebounded sharply in May, signaling improved sentiment and boosting investor optimism. In fixed income, markets also rallied as investors looked past last week’s downgrade of U.S. Treasuries by Moody’s. The 10-year Treasury yield fell 12 basis points, ending the week at 4.40%.

U.S. & Global Economy

Economic data released last week was mixed but generally better than expected. Durable goods orders declined 6.3% in April, less than the forecasted drop, while consumer confidence in May surged to 98, far exceeding expectations. Initial jobless claims ticked up slightly to 240,000, and the first revision to Q1 GDP came in at -0.2%, a modest improvement from the previous estimate. Personal income in April rose sharply by 0.8%, while consumer spending grew by 0.2%. Inflation remained subdued, with headline and core PCE indices rising just 0.1% for the month. The on-again, off-again news surrounding tariffs will likely contribute to continued volatility in both market performance and economic indicators.

Policy and Politics

Trade policy remained a focal point last week, with significant developments impacting U.S. relations with key trading partners. On May 29, the U.S. Court of International Trade ruled that President Trump’s broad tariffs, imposed on April 2 under the International Emergency Economic Powers Act (IEEPA), exceeded his authority, temporarily reducing the effective U.S. tariff rate from 15% to about 6.5%. However, the U.S. Court of Appeals for the Federal Circuit issued a stay on May 30, reinstating these tariffs pending further review, with legal filings due by June 5 and June 9. On June 1, Trump escalated tensions by announcing a doubling of steel and aluminum tariffs to 50%, accusing China of violating a trade agreement by failing to remove non-tariff barriers, stalling U.S.-China trade talks.

Global tensions continued to rise last week. In the Middle East, Israel’s war in Gaza escalated as over 12,000 Israeli reservists refused to serve, and protests in Tel Aviv called for an end to the conflict. Hamas rejected a U.S.-backed ceasefire proposal, while Israel’s military activity surged. In South Asia, a fragile May 10 ceasefire between India and Pakistan is holding, even as India suspended a key water treaty and both sides ramped up diplomatic efforts. In Ukraine, Russia launched a fresh offensive in Donbas and rejected another U.S. ceasefire attempt, further straining relations. President Trump has expressed growing frustration with President Putin over the renewed violence and lack of cooperation. Meanwhile, Chinese military exercises near Taiwan and rising threats between Iran and Israel added to the sense of global instability.

Economic Numbers to Watch This Week

- U.S. S&P final U.S. manufacturing PMI for May 2025, prior 52.3

- U.S. ISM manufacturing for May 2025, prior 48.7%

- U.S. Factory Orders for April 2025, prior 4.3%

- U.S. Job Openings for April 2025, prior 7.2 million

- U.S. S&P final U.S. services PMI for May 2025, prior 52.3

- U.S. ISM Services for May 2025, prior 51.6%

- U.S. Weekly initial jobless claims for the week of May 31, 2025, prior 240,000

- U.S. Employment report for May 2025, prior +177,000

- U.S. Unemployment rate for May 2025, prior 4.2%

This week, investors will focus on a mix of corporate earnings, labor market data, and trade developments. Earnings reports from CrowdStrike, Dollar General, Broadcom, and Lululemon are expected to provide insights into the cybersecurity, retail, semiconductor, and luxury apparel sectors. On the economic front, the U.S. May jobs report and April job openings data will be key indicators of labor market strength. Additionally, tariffs and trade policy remain fluid, with investors eager for progress on new trade deals with key partners amid ongoing uncertainty. Economic data releases related to services and manufacturing activity will also be closely monitored, including the S&P Global U.S. Manufacturing PMI and S&P Global U.S. Services PMI. Investors will also monitor remarks from Federal Reserve officials this week for updated guidance on interest rate policy amid ongoing inflation and economic growth uncertainty. If you have any questions or need additional guidance, please contact your advisor at Valley National Financial Advisors.