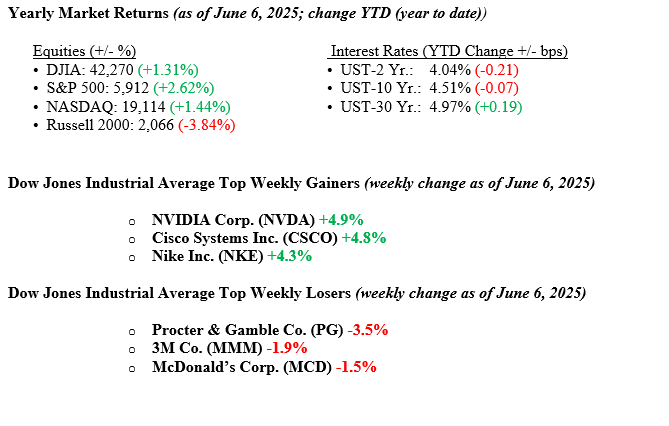

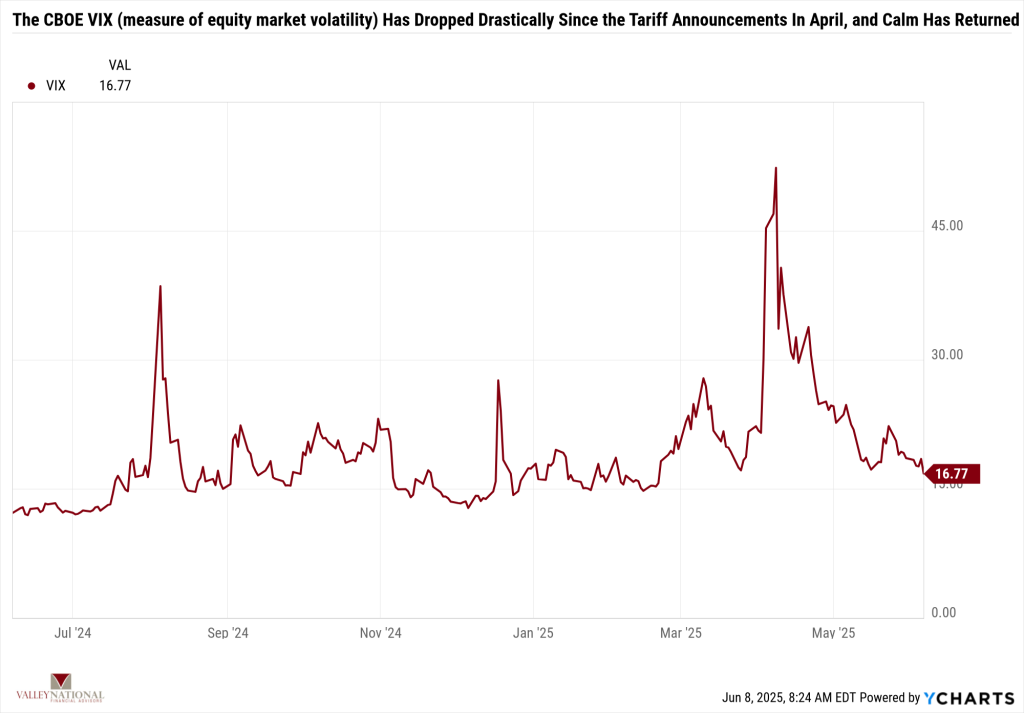

Equity markets moved higher last week, with each major index showing a gain for the week. This latest rally puts the three major indexes into positive territory year-to-date (see the numbers below). A strong labor report showing that 139,000 new jobs were created in May boosted investor confidence that the U.S. economy continues to grow and expand. We have noted that when Americans are working, they are spending, which keeps the economy moving like a freight train year after year. Lastly, see the chart below by Valley National Financial Advisers and Y Charts showing the VIX or CBOE Measure of Market Volatility. This indicates that calm has returned to the markets since the policy uncertainty that swirled around the tariff announcements in April. The 10-year Treasury yield increased 11 basis points to close the week at 4.51%.

U.S. & Global Economy

Despite volatile and sometimes conflicting economic data points, the U.S. economy demonstrates resilience and appears positioned for growth in the second quarter. Manufacturing indicators reported last week were mixed, with the S&P U.S. Manufacturing PMI slightly below expectations and the ISM Manufacturing Index remaining in contraction territory. At the same time, factory orders posted a sharp decline in April. However, strength in the services sector, reflected in the higher-than-expected S&P services PMI and a rise in job openings, points to underlying momentum. Labor market data was also mixed; ADP job gains fell short, but the official employment report showed solid hiring, stronger wage growth, and steady unemployment. A lighter import load should provide a tailwind for Q2 growth, offsetting one of the main headwinds from Q1. We remain encouraged by the economy’s resilience but acknowledge that ongoing tariff dynamics and trade negotiations remain uncertain and could impact economic growth in the months and quarters ahead.

Policy and Politics

Trade and fiscal policy tensions continued to build this past week, with several key deadlines and developments raising the stakes. Reports of stalled U.S.–China trade talks sparked concern early in the week, but a late-week call between President Trump and Xi helped ease some tensions and reopened the door for negotiations. Still, looming deadlines, including the July 9 expiration of the U.S. 90-day pause on reciprocal tariffs and China’s August 12 pause, pose significant catalysts for volatility. New investigations into pharma and semiconductor imports and a recent court ruling challenging Trump’s tariff authority have further complicated the picture. Meanwhile, the “Big Beautiful Bill,” narrowly passed by the House, has moved to the Senate, where debate has intensified over its potential impact on the federal deficit. With the debt ceiling deadline approaching fast, Treasury Secretary Bessent has urged Congress to act by mid-July, adding pressure on lawmakers to finalize a sweeping tax and spending package. Extensions on trade and fiscal fronts remain possible as officials look to buy more time to strike broader agreements.

Economic Numbers to Watch This Week

- U.S. NFIB (Small business) Optimism index for May 2025. Prior 95.8.

- U.S. Consumer Price Index for May 2025. Prior 0.2%.

- U.S. Core Consumer Price Index for May 2025. Prior 0.2%.

- U.S. Initial Weekly Jobless Claims for the week of June 7. Prior 247,000.

- U.S. Producer Price Index for May 2025. Prior –0.5%.

- U.S. Core Producer Price Index for May 2025. Prior –0.1%.

As the first-quarter earnings season winds down, this week’s calendar is relatively light, with results expected from only a few high-profile companies, including Oracle, Adobe, and Restoration Hardware. Attention will shift toward key economic data, with fresh CPI and PPI reports offering insight into whether recently announced tariffs are starting to fuel inflation. Investors will also be watching the NFIB small business confidence index for signals on how Main Street is holding up. Meanwhile, the “Big Beautiful Bill” approaches a Senate vote, and financial markets will closely monitor any updates or changes by Congress. With the Fed in its pre-FOMC blackout period ahead of the June 17–18 policy meeting, markets must rely on data alone to assess the odds of any rate moves, which currently lean toward no change. If you have any questions or need additional guidance, please get in touch with your advisor at Valley National Financial Advisors.