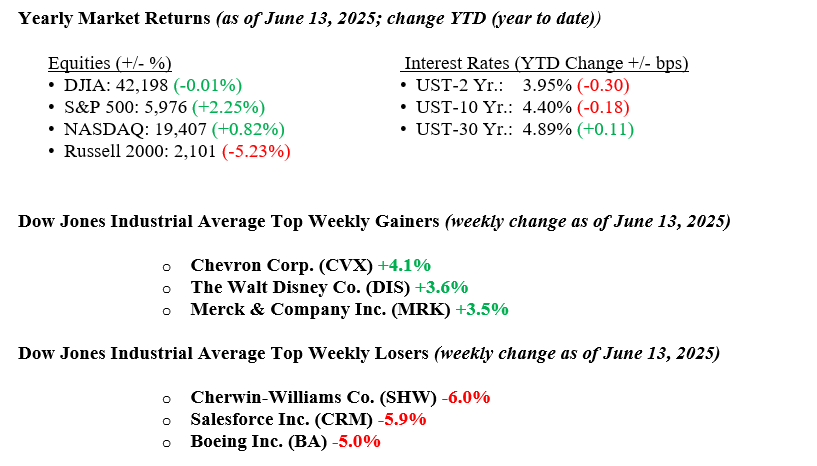

Last week, U.S. equity markets swung between gains and losses: the S&P 500, after rallying early, finished down about 0.25%, the Dow held flat, and the Nasdaq fell 0.5%. Geopolitical flare-ups after Israel’s strike on Iran sent oil prices up 8% and drove investors toward gold and the dollar. However, a surprisingly strong consumer sentiment reading on Friday briefly lifted optimism. Meanwhile, better-than-expected small business optimism, with the NFIB index rising to 98.8 in May, signaled improved sentiment among Main Street businesses. Alongside tame inflation readings, with CPI and PPI rising less than expected in May, this has bolstered hopes that the Fed may begin cutting rates later this year. Despite late-week jitters, the S&P 500 is still up around 20% from its April 8 low, showing resilience amid tariff and China-trade headwinds. After large-scale military actions by Israel and Iran, there was a massive flight to quality, and as a result, U.S. Treasury bonds rallied. The 10-year Treasury yield decreased 11 basis points to close the week at 4.40%.

U.S. & Global Economy

Economic data from last week showed signs of easing inflationary pressures alongside improved business and consumer sentiment. The NFIB small business optimism index rose to 98.8 in May, beating expectations and marking a notable rebound from April’s 95.8. Inflation data came in softer than anticipated, with headline and core CPI increasing just 0.1% in May, below forecasts and previous readings. Similarly, PPI and core PPI each rose 0.1%, also under expectations, reinforcing a trend of moderating price pressures. Initial jobless claims remained steady at 248,000, in line with estimates. Meanwhile, consumer sentiment jumped sharply to 60.5 in early June, a sign of growing confidence amid cooling inflation. However, a recent spike in oil prices poses a potential upside risk to future inflation, complicating the disinflationary narrative if energy costs continue to rise.

Policy and Politics

Last week, tensions between Israel and Iran escalated sharply. Israel launched significant airstrikes on Iranian nuclear and military sites, saying Iran was close to building a nuclear weapon. In response, Iran fired missiles and drones at Israeli targets. The conflict caused damage and casualties on both sides, raising fears of a wider regional war.

U.S. and Chinese officials met in London last week to ease trade tensions. They agreed to revive a trade truce, but the details are vague, and negotiations remain uncertain. U.S. Treasury Secretary Bessent suggested the U.S. might extend a pause on tariffs for countries negotiating in “good faith,” though no firm decisions were made.

The One Big Beautiful Bill Act is facing intense debate and delays in the Senate, with a vote now likely pushed to late June. Supporters claim it will boost the economy, but critics warn it could cost low-income families $1,600 annually. Reports highlight a massive $11 trillion gap in deficit projections, fueling concerns, while accusations of misleading claims intensify political tensions around the bill’s future.

Economic Numbers to Watch This Week

- U.S. Empire State manufacturing survey for June 2025. Prior reading –9.2.

- U.S. Retail Sales for May 2025. Prior reading +0.1%

- U.S. Homebuilder Confidence Index for June 2025. Prior level 34.

- U.S. FOMC Interest Rate Decision. No Change expected.

- U.S. Philadelphia Fed manufacturing survey for June 2025. Prior reading –4.0

- U.S. Leading economic indicators for May 2025. Prior reading –1.0%.

Markets are navigating a complex mix of global risks and policy shifts, but healthy underlying fundamentals continue to offer support. While the Israel–Iran conflict briefly rattled markets on Friday, the S&P 500 remains up over 20% since early April, helped by solid corporate earnings, resilient consumer demand, and easing trade tensions. Economic data has stayed broadly positive, and investors are increasingly optimistic about the potential for more supportive fiscal and monetary policy in 2026. At this week’s Fed meeting, rates are expected to remain steady, with updated projections likely to point to a gradual path toward easing later this year. Meanwhile, progress in U.S.-China trade talks and the possible extension of a tariff pause reflect a more constructive tone, even if details are still emerging. Overall, despite near-term uncertainty, markets are looking ahead with cautious confidence. If you have any questions or need additional guidance, please contact your advisor at Valley National Financial Advisors.