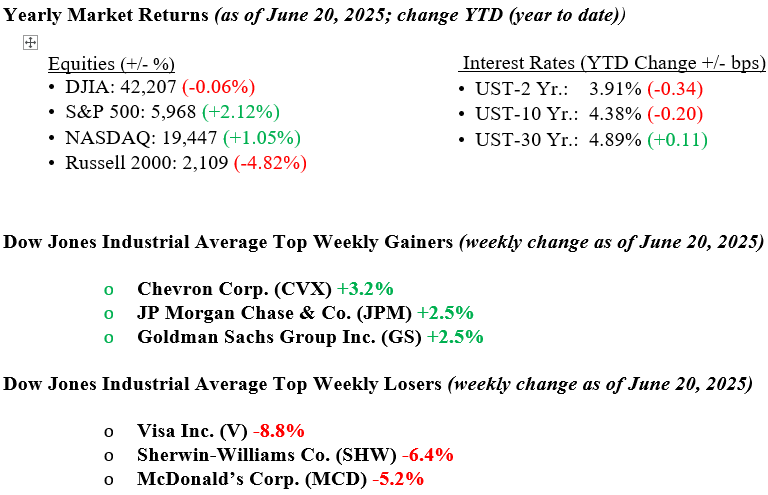

Last week, markets were calm early but became more cautious as several risks emerged. Stocks ended slightly lower after weaker-than-expected retail sales, impacted by earlier pre-tariff buying, and a drop in housing starts raised concerns about consumer strength. The Federal Reserve, as expected, kept interest rates unchanged and signaled a patient approach in the future, mentioning slightly elevated inflation risk and slower growth. Bond yields initially dipped due to safe-haven buying before rising later in the week. Oil prices surged over 10%, driven by increasing tensions in the Middle East, especially after the U.S. launched a military strike on Iran’s nuclear facilities on June 21. The move increased fears of a broader conflict and added uncertainty to global markets. While investors watched these developments closely, last week was notably quiet on the trade front, with no major updates to ongoing negotiations. The 10-year Treasury yield decreased two basis points to close the week at 4.38%.

U.S. & Global Economy

The recent economic data showed a mixed and confusing picture of the U.S. economy. Several reports came in weaker than expected, including retail sales, which dropped in May and suggested that consumer spending may have been pulled forward earlier in the year due to tariff concerns. Manufacturing remained weak, with the Empire State and Philadelphia Fed surveys staying in negative territory. The housing market also showed signs of softening, with fewer housing starts and slightly lower building permits. Homebuilder confidence dipped as well. Jobless claims were steady, primarily pointing to a labor market holding up but not especially strong. The Federal Reserve kept interest rates unchanged and acknowledged lingering inflation pressures and slower expected growth. Overall, the data remains hard to read clearly, especially with trade-related uncertainty and shifting business and consumer behavior still playing a role.

Policy and Politics

- The conflict between Israel and Iran escalated rapidly last week. After Iran launched a major missile and drone attack on several Israeli cities, causing civilian casualties and damaging infrastructure, Israel responded with a large-scale air and drone campaign targeting over one hundred Iranian military and nuclear sites. The situation worsened when, on June 21, the U.S. joined the fight by striking Iranian nuclear facilities with B-2 bombers and Tomahawk missiles. These developments sparked fears of a broader regional war, causing oil prices to surge due to concerns about supply disruptions. Investors responded by shifting into safer assets like gold and U.S. Treasuries, while stock markets pulled back slightly amid the rising geopolitical uncertainty.

- Alongside escalating tensions in the Middle East, two significant developments heightened global uncertainty. In Washington, Senate Republicans unveiled their “Big Beautiful Bill,” proposing deeper Medicaid cuts, a sharply reduced SALT deduction cap compared to the House plan, and fewer rollbacks of clean energy tax credits. The bill has already faced pushback from moderate Republicans and awaits a Senate ruling, with a vote around July 4. Meanwhile, Russian President Putin declared “all of Ukraine is ours” in the latest blow to peace talks.

Economic Numbers to Watch This Week

- U.S. S&P flash services PMI for June 2025. Prior reading 53.7.

- U.S. S&P flash manufacturing PMI for June 2025. Prior reading 52.0.

- U.S. Existing Home Sales for May 2025. Prior level 4.0 million.

- U.S. Consumer Confidence Index for June 2025. Prior reading 98.0.

- U.S. New Home Sales for May 2025. Prior level 743,000.

- U.S. Initial Jobless Claims for week ending June 21, 2025. Prior reading 245,000.

- U.S. Durable Goods Orders for May 2025. Prior reading –6.3%.

- U.S. GDP (Second Estimate) for Q1 2025. Prior reading –0.2%.

- U.S. Pending Home Sales for May 2025. Prior reading –6.3%.

- U.S. Consumer Sentiment (Final) for June 2025. Prior reading 60.5.

- U.S. Personal Income for May 2025. Prior reading +0.8%.

- U.S. Personal Spending for May 2025. Prior reading +0.2%.

- U.S. PCE Price Index for May 2025. Prior reading +0.1%.

- U.S. Core PCE Price Index for May 2025. Prior reading +0.1%.

Markets head into the week facing a complex mix of global risks and shifting policy signals. A heavy slate of economic data is on tap, but readings may be hard to interpret due to recent tariff-related distortions in consumer and trade activity. Geopolitical concerns remain front and center, with investors watching closely for any potential retaliation from Iran following last week’s U.S. airstrikes on its nuclear sites, which could further unsettle energy markets and broader sentiment. At the same time, global trade developments and corporate headlines remain key focus areas, as uncertainty in these areas continues to weigh on the economic outlook. Investors will also pay close attention to any follow-up commentary from Federal Reserve officials after the central bank decided to hold interest rates steady, looking for clues on the path ahead. If you have any questions or need additional guidance, please contact your advisor at Valley National Financial Advisors.