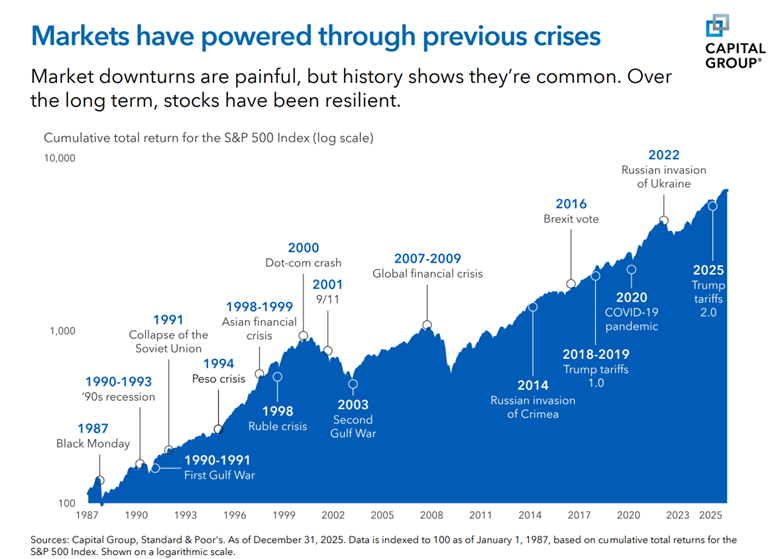

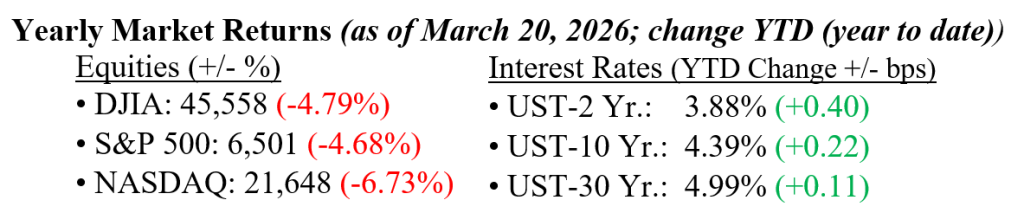

U.S. equities moved lower for the week ending March 20, with the S&P 500 declining roughly 1.9%, the Dow Jones Industrial Average falling about 2.1%, and the Nasdaq Composite slipping approximately 2.1%. Markets continued to trade under the weight of escalating global conflict, particularly in the Middle East, where ongoing disruptions to energy flows and elevated oil prices are injecting significant short-term uncertainty into the outlook. That uncertainty, not a deterioration in underlying fundamentals, has been the primary driver of volatility. Economic data over the week continued to point toward slower, but still positive, growth, with inflation remaining somewhat sticky. Treasury yields moved higher, with the 10-year rising further into the mid-4% range, as markets pushed out rate-cut expectations amid firmer inflation risks tied to energy prices. See Chart 1 below from Capital Group showing how markets prevailed through previous periods of uncertainty and peril. While geopolitical tensions are clearly impacting sentiment and near-term market direction, the long-term foundation of the U.S. economy, supported by a resilient consumer, solid corporate balance sheets, and structural advantages such as energy independence, remains intact.

U.S. & Global Economy

- Economic data for the week ending March 20 continued to paint a mixed but generally stable picture. The more important development this week was the market’s reaction to rising energy prices, which is beginning to push inflation expectations higher even without new hard data. On the growth side, incoming data remains consistent with a slower expansion, no sharp deterioration, but clearly less momentum than late 2025. Housing data was mixed, with existing home sales holding relatively steady after recent gains, while new construction indicators showed some volatility but remain off their lows. The labor market continues to provide a stabilizing force; weekly jobless claims continue to hold at a historically low level, indicating no broad-based layoffs. Our more salient concern comes from the risk of a prolonged Middle East War that impacts global energy prices and relative global economic stability.

Policy and Politics

- The U.S.-Israeli war with Iran remained the main global macro story this week, keeping investors focused on geopolitics, energy, and trade. The effective closure of the Strait of Hormuz and attacks on regional energy infrastructure have driven a major supply shock, with oil prices moving above $100 per barrel and, in some markets, substantially higher. That has reinforced concerns that persistently elevated energy prices could weigh on global growth while keeping inflation pressure alive, especially in more energy-import-dependent parts of Europe and Asia. The International Energy Agency has already approved a record 400 million-barrel release from strategic reserves, but analysts caution that the move may only partially offset the disruption if shipping constraints persist. On trade, the Trump Administration also opened new unfair-trade investigations into major trading partners as it seeks to rebuild tariff leverage, adding another layer of policy uncertainty. For markets, the backdrop remains one of elevated geopolitical risk, energy volatility, and renewed trade friction, all of which should keep sentiment cautious in the near term.

It’s shaping up to be a relatively quiet but still meaningful week for markets, with a lighter economic calendar putting more weight on a few key catalysts. A big focus will be on commentary from six Federal Reserve officials speaking throughout the week, which could offer fresh clues on the timing and likelihood of rate cuts. On the data front, attention will likely center on the March consumer sentiment reading, as investors look for signs of how resilient the U.S. consumer remains. Earnings from Paychex and Carnival Cruise Line should also provide useful insight into labor market conditions and discretionary spending trends. That said, the dominant driver of market sentiment will likely remain geopolitical, with continued focus on the Iran conflict and its ripple effects on oil prices, inflation expectations, and interest rate outlooks. Your team at Valley National Financial Advisors is here to help you navigate these developments and answer any questions you may have.

Economic Numbers to Watch This Week

- U.S. Productivity (revision) for Q4 2025, prior 2.8%

- U.S. S&P Flash U.S. Services PMI for March 2026, prior 51.7

- U.S. S&P Flash U.S. Manufacturing PMI for March 2026, prior 51.6

- U.S. Import Price Index for February 2026, prior 0.2%

- U.S. Initial Jobless Claims for week ending March 21, 2026, prior 205,000

- U.S. Consumer Sentiment (final) for March 2026, prior 55.5

Please review Important Disclosure Information set forth in the last section of this web site.