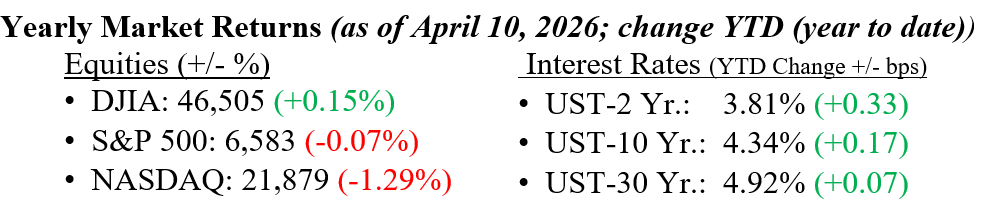

U.S. stocks posted strong gains for a second straight week, as news of a two-week ceasefire and plans for direct U.S.–Iran negotiations sparked a broad risk-on rally. This helped ease concerns over energy supply disruptions and pushed oil prices lower. Furthermore, the rally reinforced signs that the earlier theme of a broadening market rally beyond just mega-cap tech was reasserting itself, alongside renewed strength in AI-related stocks. Technology and AI drove gains, while energy lagged sharply amid weaker crude prices. As a result, all major indexes finished higher, with the Nasdaq leading the way. However, while a definitive plan for safe travel through the Strait of Hormuz remains uncertain, overall efforts toward de-escalation were viewed as a positive sign. Looking ahead, investors will continue to monitor the durability of the ceasefire and broader geopolitical risks in the new week. In addition, Treasury markets also gained as volatility eased. The 10-year U.S. Treasury ended the week 13 basis points lower to close the week at 4.31%.

U.S. & Global Economy

- Geopolitical tensions from the Iran war are likely to create some challenging near-term economic data points, particularly through higher energy prices, though the expectation is that these effects remain temporary and do not materially alter the longer-term growth trajectory. Against that backdrop, U.S. inflation data showed CPI rising 3.3% year over year in March, up from 2.4% in February, driven largely by a surge in gasoline prices, while core CPI rose 2.6%. Core PCE inflation eased slightly to 3.0% year over year in February, and personal income declined 0.1% after a 0.4% gain in January. GDP growth for Q4 2025 was revised down 0.7% to 0.5%, reflecting weaker investment. ISM services eased to 54.0 in March but remained in expansion territory, with elevated price pressures, while consumer sentiment fell sharply to 47.6 in April as inflation expectations rose to 4.8%. Despite these pressures, labor market conditions remain relatively steady, and companies including Walmart, Delta, and Levi’s continue to point to resilient consumer demand, while Fed’s Mary Daly said U.S. economic fundamentals remain in a “good place.”

Policy and Politics

- U.S. political developments last week centered on the conflict with Iran. The Trump administration and Iran agreed to a two-week ceasefire and plans to reopen the Strait of Hormuz, while a U.S. delegation, led by Vice President JD Vance, traveled to Islamabad for talks aimed at ending the six-week conflict, though the negotiations did not yield any meaningful progress. On the domestic front, House Republicans blocked a Democratic effort to limit Trump’s war powers. The partial government shutdown extended past 50 days, with funding for the Department of Homeland Security still stalled despite a Senate-passed bill. Trump said he would resume pay for DHS employees, though full compensation depends on the restoration of funding. On trade, tariffs remained in focus. A legal challenge to Trump’s revised 10% global tariff was heard in court, and a new proclamation raised tariffs on steel, aluminum, and copper to 50%. Trump also threatened additional tariffs on countries supplying weapons to Iran, though the legal basis for those measures remains uncertain.

Q1 2026 earnings season kicks off this week, with several major companies set to report results. Key bank earnings include Goldman Sachs on Monday, followed by JPMorgan Chase, Citigroup, Wells Fargo, and BlackRock on Tuesday, and Morgan Stanley and Bank of America reporting on Wednesday. Investors will also watch Johnson & Johnson for healthcare demand trends and Netflix for consumer subscription momentum later in the week. FactSet estimates point to S&P 500 earnings growth of 12.5% year over year. Alongside earnings, markets remain focused on the durability of the recent Iran War ceasefire and on ongoing geopolitical risks to energy infrastructure and global supply chains, which continue to support a modest risk premium and could drive volatility. Your team at Valley National Financial Advisors is here to help you navigate these developments and answer any questions as conditions evolve.

Economic Numbers to Watch This Week

- U.S. Existing Home Sales for March 2026, prior 4.09 million

- U.S. NFIB Small Business Optimism Index for March 2026, prior 98.8

- U.S. Producer Price Index (PPI) for March 2026, prior 0.7%

- U.S. Core Producer Price Index (Core PPI) for March 2026, prior 0.5%

- U.S. Import Price Index for March 2026, prior 1.3%

- U.S. Import Price Index (Ex-Fuel) for March 2026, prior 1.1%

- U.S. Empire State Manufacturing Survey for April 2026, prior -0.2

- U.S. Home Builder Confidence Index for April 2026, prior 38

- U.S. Initial Jobless Claims for week of April 11, 2026, prior 219,000

- U.S. Philadelphia Fed Manufacturing Survey for April 2026, prior 18.1

Please review Important Disclosure Information set forth in the last section of this web site.