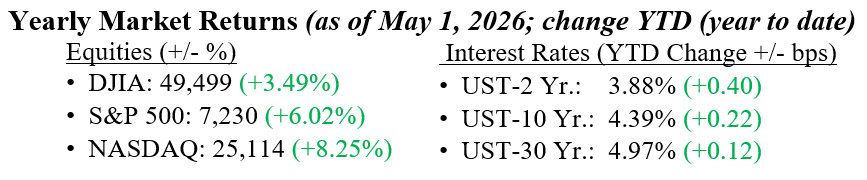

Equity markets finished the week on a modestly positive note, with the S&P 500 up roughly 0.9%, the Dow Jones Industrial Average up 0.5%, and the Nasdaq Composite leading with a gain of about 1.1%. Geopolitics remained in focus, but tentative progress in U.S.–Iran discussions helped stabilize sentiment. First-quarter earnings continue to come in better than expected, with a clear divide between strength in semiconductor/AI-driven names and more measured trends in software. Industrials also remained a bright spot, supported by solid execution and steady demand. On the macro front, the U.S. economy once again showed resilience, with a healthy 2.0% GDP reading underscoring that consumer and business spending continue despite elevated uncertainty. Oil prices increased modestly to the low $100s this week, reflecting continued concern due to Middle East tensions. In fixed income, Treasury yields edged higher, with the 10-year U.S. Treasury rising 5 basis points to 4.37%, as markets continue to push out the timing of potential Federal Reserve rate cuts.

U.S. & Global Economy

- We remain skeptically optimistic on the market and the economy, supported by two core fundamentals: consumers are working and spending and corporate earnings continue to rise. Recent economic data has been better than expected, reinforcing the resilience of the U.S. economy. Retail sales remain firm, and consumer confidence for April came in stronger than expected. The labor market remains healthy, with last week’s claims for unemployment insurance declining to 189,000 from 215,000 the previous week, and hiring trends remain steady. However, monetary policy is becoming more complex. The Federal Reserve held rates steady last week but showed increasing internal disagreement among voting members. New Fed Chairman Kevin Warsh is set to take over as soon as June. Markets are beginning to factor in potential shifts in monetary policy. Taken together, and supported by generally constructive corporate commentary this earnings season, the data points to a durable consumer and a fundamentally solid economic backdrop, even as policy uncertainty rises.

Policy and Politics

- U.S. policy risks eased modestly this week as several key overhangs began to clear. Geopolitically, tensions with Iran stabilized, with ceasefire conditions holding and diplomatic engagement continuing, reducing the risk of near-term escalation. Meanwhile, on the domestic front, Washington resolved the government shutdown, restoring funding and removing a source of immediate economic uncertainty. Additionally, uncertainty around the Federal Reserve transition has lessened, as recent legal challenges regarding Chair Jerome Powell’s position have been resolved, providing greater clarity on leadership continuity. Turning to trade, the administration continues to advance a 10% global baseline tariff framework while maintaining elevated pressure on China. Taken together, the policy backdrop remains complex, but the tone has shifted modestly toward the constructive as near-term risks begin to stabilize.

Investors are heading into another busy week, highlighted by a full slate of earnings from companies including Advanced Micro Devices, Super Micro Computer, Uber Technologies, Walt Disney Company, Airbnb, Shopify, and McDonald’s, which should provide further clarity on demand trends across technology, consumer, and travel. In addition, investors will be keeping a close eye on the April jobs report, which is expected to offer an updated read on labor market conditions. At the same time, oil prices and developments in Iran remain key drivers of sentiment. Despite a steady stream of noisy headlines, the fundamental backdrop remains supportive. Economic growth is holding up, earnings are broadly solid, and the consumer continues to spend. These conditions have historically rewarded disciplined, long-term investors. Periods like this can create short-term volatility, but they do not alter the core principles of successful investing: staying invested, remaining diversified, and maintaining a long-term focus on wealth accumulation. Please contact your partners at Valley National Financial Advisors for any questions you may have.

Economic Numbers to Watch This Week

- U.S. Factory Orders for March 2026, prior 0.5%

- U.S. Job Openings for March 2026, prior 6.9 million

- U.S. New Home Sales (Delayed Report) for February 2026, prior 587,000

- U.S. S&P Final Services PMI for April 2026, prior 51.3

- U.S. ISM Services Index for April 2026, prior 54.0%

- U.S. ADP Employment for April 2026, prior 62,000

- U.S. Initial Jobless Claims for May 2, 2026, prior 189,000

- U.S. Productivity for Q1 2026, prior 1.8%

- U.S. Employment Report for April 2026, prior 178,000

- U.S. Unemployment Rate for April 2026, prior 4.3%

- U.S. Hourly Wages for April 2026, prior 0.2%

- U.S. Consumer Sentiment (Preliminary) for May 2026, prior 49.8

Please review Important Disclosure Information set forth in the last section of this web site.