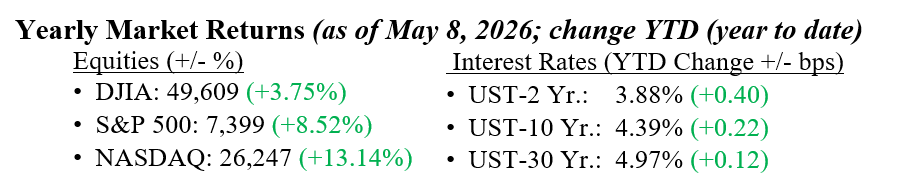

Equity markets continued to push higher last week, with the S&P 500 gaining 2.4% and the Nasdaq surging 4.5%. Both indexes extended their winning streaks to six consecutive weeks and reached fresh record highs, while the Dow Jones Industrial Average finished modestly higher. Hopes for easing tensions with Iran, combined with another strong week of corporate earnings, continued to support investor sentiment and keep momentum firmly tilted toward equities. Technology and AI-related companies once again led the rally, highlighted by the remarkable strength in semiconductors, with the SOX semiconductor index posting an extraordinary 57% gain over the last six weeks. Economic data also continued to point to a resilient U.S. economy, reinforcing confidence that growth remains on a solid footing despite ongoing uncertainty around the Iran War. Meanwhile, oil prices and Treasury yields remained volatile as investors continued to monitor geopolitical developments, inflation pressures, and the outlook for Federal Reserve policy. The 10-year U.S. Treasury yield ended the week at 4.39%, essentially unchanged from the prior week.

U.S. & Global Economy

- Last week’s economic data showed a resilient U.S. economy, even as consumer sentiment fell. The labor market remained strong, jobless claims stayed low, and nonfarm payrolls rose by 115,000 in April, the best two-month hiring stretch since 2024. Private payroll gains beat expectations; factory orders and construction spending also rose, aided by continued investment in AI infrastructure. However, there were signs of moderation: productivity growth slowed, and tech-sector layoffs increased. Consumer confidence remained weak as higher gas prices and tariff concerns drove the University of Michigan’s index to a record low of 48.2. This underscores the gap between strong economic data and consumer sentiment.

- U.S. policy and political developments last week focused on trade and geopolitics. The Trump administration announced plans to raise tariffs on European Union cars and trucks from 15% to 25%. Officials cited concerns that the EU had failed to uphold parts of last year’s trade agreement. The tariff move also appeared tied to broader tensions over Europe’s stance on the Iran conflict. Attention then shifted to the upcoming Trump-Xi summit in Beijing. The agenda is expected to include trade, export controls, Taiwan, rare-earth minerals, and the Iran war. Markets are closely watching for signs of improving U.S.-China relations, such as the possibility of a major Boeing aircraft order from China. However, expectations for broader geopolitical breakthroughs remain modest. Meanwhile, developments with Iran remained fluid. Tehran indicated it was reviewing a U.S. peace proposal to end the conflict, and both sides signaled cautious openness to an agreement.

Looking ahead, earnings season is nearly over. About 90% of S&P 500 companies have reported. Notable earnings to come include Cisco, Toyota Motor, and Alibaba. This season has been strong: 84% of companies delivered positive EPS surprises, and 80% beat revenue estimates. Q1 earnings are up 27.7% year over year, the fastest growth since late 2021 and well over initial forecasts. Most sectors have seen upward revisions, with ten sectors now reporting better earnings estimates and widespread beats. Attention will now turn from earnings to key economic data, including new CPI, PPI, and retail sales numbers, which will shape growth and expectations for Federal Reserve policy. The recent equity rally has been driven largely by large-cap tech and AI stocks. Investors are watching to see if this momentum spreads to other sectors soon. Please contact your partners at Valley National Financial Advisors for any questions you may have.

Economic Numbers to Watch This Week

- U.S. Existing Home Sales for April 2026, prior 4.0 million

- U.S. NFIB Small Business Optimism Index for April 2026, prior 95.8

- U.S. Consumer Price Index (MoM) for April 2026, prior 0.9%

- U.S. Core CPI (MoM) for April 2026, prior 0.2%

- U.S. Producer Price Index (MoM) for April 2026, prior 0.5

- U.S. Core PPI (MoM) for April 2026, prior 0.2%

- U.S. Retail Sales for April 2026, prior 1.7%

- U.S. Initial Jobless Claims for May 9, 2026, prior 200,000

- U.S. Import Price Index for April 2026, prior 0.8%

- U.S. Empire State Manufacturing Survey for May 2026, prior 11.0

Please review Important Disclosure Information set forth in the last section of this web site.