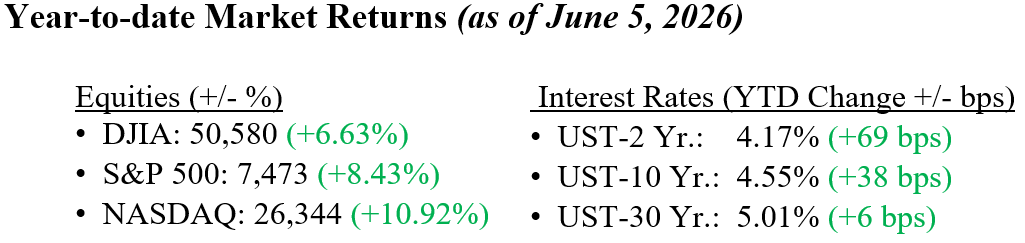

U.S. equities pulled back sharply last week as stretched technology and AI-related stocks came under pressure, with the NASDAQ falling 4.7%, the S&P 500 declining 2.6%, and the Dow slipping 0.3%. While the sell-off interrupted a strong multi-week rally, year-to-date returns remain solid, and the broader backdrop remains constructive. The May jobs report showed the economy added 172,000 jobs, well above expectations, while unemployment held steady at 4.3%, reinforcing the view that the labor market remains resilient. Consumers are still facing pressure from higher gasoline prices and elevated interest rates, but spending trends continue to suggest they are weathering the storm reasonably well. Treasury yields moved higher after the stronger jobs data, with the 10-year U.S. Treasury yield rising to roughly 4.55%. Overall, last week’s volatility appears more like a normal reset after a powerful rally than a change in the longer-term trend.

U.S. & Global Economy

- Recent economic data continued to reflect a resilient, though moderating, U.S. economy. Inflation remains somewhat sticky and above the Federal Reserve’s long-term target, keeping Fed officials cautious regarding the timing of future interest rate cuts. At the same time, consumer spending continues to hold up reasonably well despite slower income growth and pressure from higher borrowing costs. Economic growth has cooled from last year’s unusually strong pace, but overall activity remains consistent with a stable expansion rather than an imminent recession. Encouragingly, manufacturing activity has shown signs of improvement, supported by durable goods demand and continued investment tied to artificial intelligence, infrastructure, and reshoring initiatives. Meanwhile, weekly jobless claims remain at relatively healthy levels, reinforcing the view that the labor market continues a solid footing despite ongoing workforce reduction announcements across parts of the technology sector. Globally, economic conditions remain uneven, with sluggish growth in Europe and softer consumer demand in China. Overall, while pockets of softness remain, the global economy continues to demonstrate resilience despite higher interest rates and geopolitical uncertainty.

Policy and Politics

- Geopolitical developments remained an important focus for investors last week. On the Iran front, U.S. and Iranian negotiators reached a tentative 60-day understanding to extend the ceasefire and continue nuclear discussions, although several major issues remain unresolved, including uranium enrichment and Iran’s existing nuclear stockpile. While administration officials described the talks as constructive, no final agreement has been approved. Meanwhile, Treasury Secretary Bessent stated that the U.S. is not rushing to extend its tariff truce with China beyond November, though he characterized the overall relationship as stable and noted reasonable progress on commitments related to critical minerals. In Ukraine, battlefield conditions remain fluid, with continued drone strikes, shifting front-line momentum, and no clear path toward a near-term resolution. Overall, geopolitical risks remain elevated, although markets continue to demonstrate an ability to look through much of the headline noise.

Investor focus is shifting from earnings season to upcoming economic data, Federal Reserve policy, and geopolitical events. First-quarter earnings remain broadly encouraging, with technology, communication services, and consumer-related firms outperforming, driven by artificial intelligence and solid consumer demand. The outlook now depends on labor market and inflation data, which will influence interest rates and the overall economy. We are also monitoring the U.S.-Iran ceasefire, as renewed tensions could increase volatility via higher oil prices. We will be watching the results of two upcoming events: the SpaceX IPO (June 12) and new Fed Chairman Kevin Warsh’s first FOMC meeting (June 16-17). These two events could set the tone for the markets going forward, regardless of their actual immediate impact. Despite these uncertainties, resilient economic growth, solid corporate earnings, and continued innovation support a constructive long-term view for investors. In periods of heightened uncertainty, the team at Valley National Financial Advisors remains focused on helping clients stay disciplined and aligned with their long-term goals.

Economic Numbers to Watch This Week

- U.S. NFIB Optimism Index for May 2026, prior 95.9

- U.S. Trade Balance for April 2026, prior -$60.3 billion

- U.S. Existing Home Sales for May 2026, prior 4.02 million

- U.S. Consumer Price Index (CPI) for May 2026, prior 0.6%

- U.S. Core CPI for May 2026, prior 0.4%

- U.S. Initial Jobless Claims for June 6, 2026, prior 225,000

- U.S. Producer Price Index (PPI) for May 2026, prior 1.4%

- U.S. Core PPI for May 2026, prior 0.6%

- U.S. Consumer Sentiment (Preliminary) for June 2026, prior 44.8

Please review Important Disclosure Information set forth in the last section of this web site.