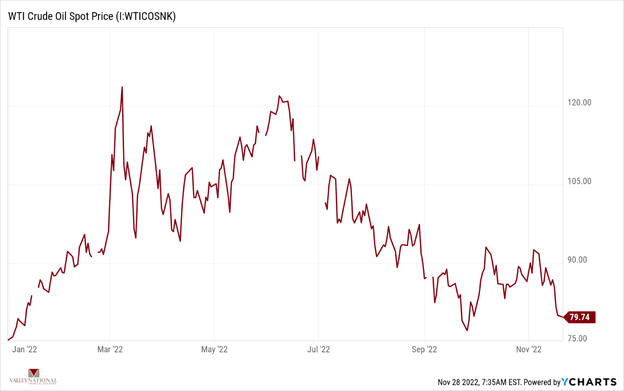

Equity markets posted gains across all three major indexes with the Dow Jones Industrial Average once again leading the way with a +2.39% gain for the week. The S&P 500 Index rose by +2.02% and the tech-heavy NASDAQ, made up of stocks that historically favor low interest rates, rose by only +0.73%. Interest rates fell last week when the minutes of the November 2022 FOMC (Federal Open Markets Committee) meeting indicated policy makers had agreed that a “slowing in the pace of future interest rates would soon be appropriate.” The 10-Year U.S. Treasury note fell by 15 basis points to close the week at 3.68%. Lastly, as we discussed last week, oil, a key economic component and critical ingredient in industrial production, fell to $76.28 for a barrel of Brent crude oil. China COVID-19 lockdowns and related slowing economic conditions in China contributed to oil’s falling price.

Global Economy

As mentioned above, the aggressive COVID-19 lockdowns in China are reverberating across the global economy impacting both the supply and demand components. On an inflationary front, China’s lessening demand for industrial products like oil and rare earth elements used in the production of batteries and solar panels, will certainly aid the global efforts to combat inflation. (See Chart 1 below from Valley National and Y Charts showing the price of oil year-to-date 2022). However, China is a key supplier of goods such as iPhones, TVs and of course, solar panels all of which remain in high demand globally. The news from China about social unrest and protests in several major cities including Beijing due to their aggressive zero-COVID policy weighs heavily on the timing of China’s eventual emergence from the pandemic.

COVID lockdowns may seem like a “China Problem,” but China currently remains the crossroads for the global supply chain and any unrest in their supply chain will percolate through the world’s economy as we saw in 2020-21. However, many countries, importantly the United States, learned from this event and have begun “on-shoring” their production. For example, Intel is building a $20 billion chip manufacturing facility in Ohio and Ford is building a $5.6 billion battery and vehicle manufacturing campus in Tennessee. We believe that investment in U.S. manufacturing is critical to the future of growth and stability of our economy, and that this wave of internal investment and innovation is just starting.

Policy and Politics

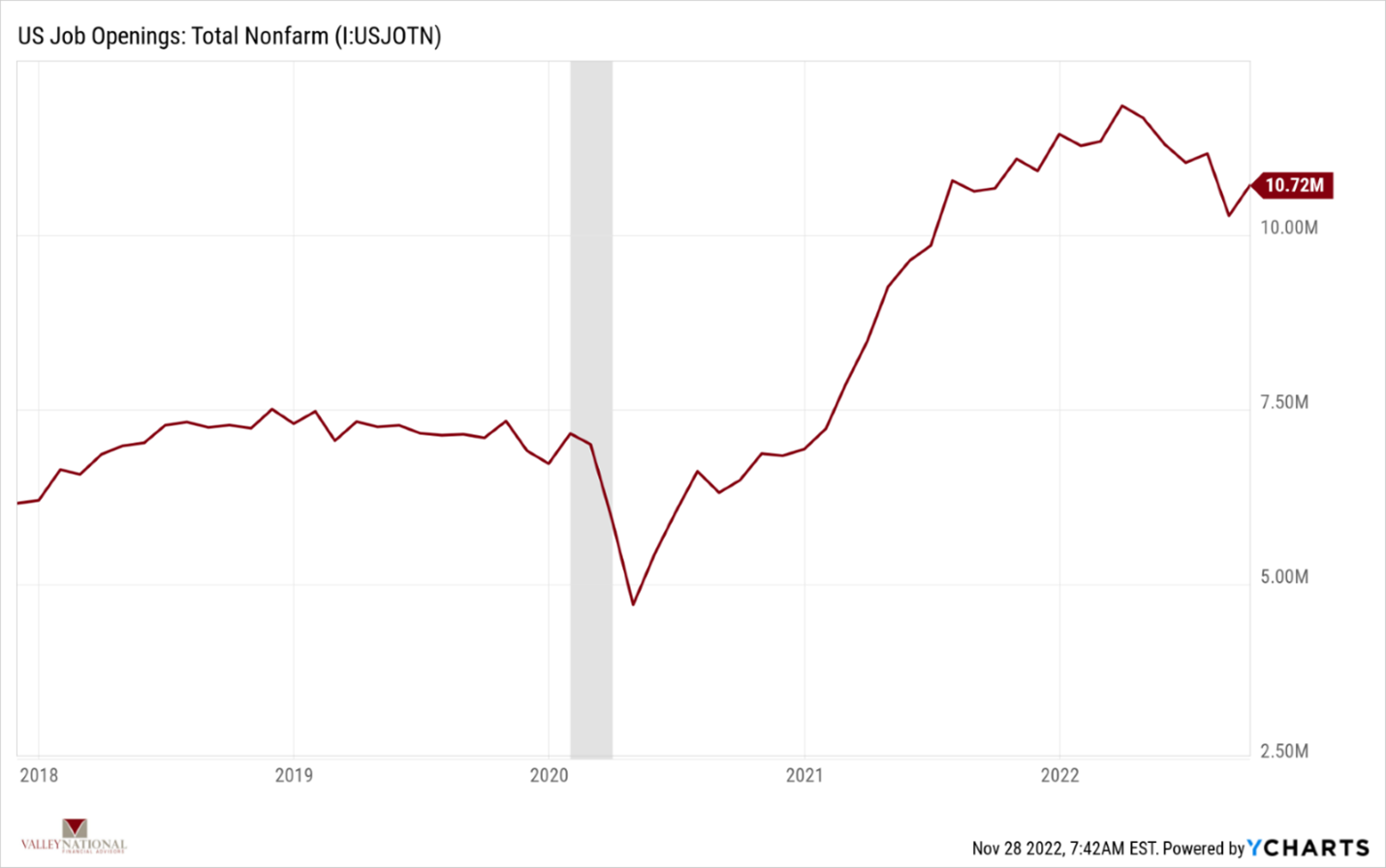

This week, the Bureau of Labor Statistics releases the U.S. Job Openings figure for October 2022 (gathered from the Job Openings and Labor Turnover Survey – JOLTS). The September figure showed 10.72 million job openings, an increase from August of 10.28 million openings. (See Chart 2 below from Valley National Financial Advisors and Y Charts). The so-called JOLTS survey is known to be a closely watched data point by the FOMC because it is an important measure of the tightness in the job market. A softening labor market would certainly help to ease inflationary pressures such as wage growth.

What to Watch

- While not an economic indicator, the unraveling of the FTX cryptocurrency mess continues to hold a pall over the entire cryptocurrency market as uncertainty abounds. Markets hate uncertainty.

- Case-Shiller Composite 20 Home Price Index Year-over-Year for September 2022 released 11/29/22 (prior +13.11%)

- U.S. Job Openings: Nonfarm for October 2022, released 11/30/22 (prior 10.72M)

- U.S. PCE (Personal Consumption Expenditures) Price Index Year-over-Year for October 2022, released 12/1/22 (prior +6.24%)

Summary

While problems remain in the economy, including such risks as China-influenced supply disruptions and inflation, we are seeing seeds of a turnaround and a lessening in inflationary pressures such as falling oil prices. Meanwhile, the Dow Jones Industrial Average closing at 34,347 as of 11/25/22, has rallied +20% since bottoming on September 29, 2022, at 28,726. Stock markets have historically been excellent predictors of future economic results. Further, the VIX (the CBOE Volatility Index) fell again last week to 20.4, down from a recent high of 33.6 on October 11, 2022. The VIX is used as a barometer for fear and uncertainty in the future markets. As we mentioned last week, the time between Thanksgiving and Christmas is typically a quiet, calm time on Wall Street and the VIX is certainly sending that message. We would love to simply say keep calm—but rather we say keep vigilant and focus on matters that grow wealth over extended periods of time.