By: Chief Investment Officer, William Henderson

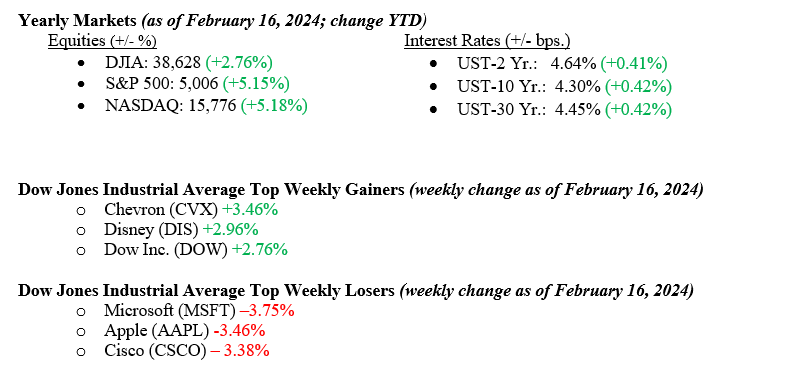

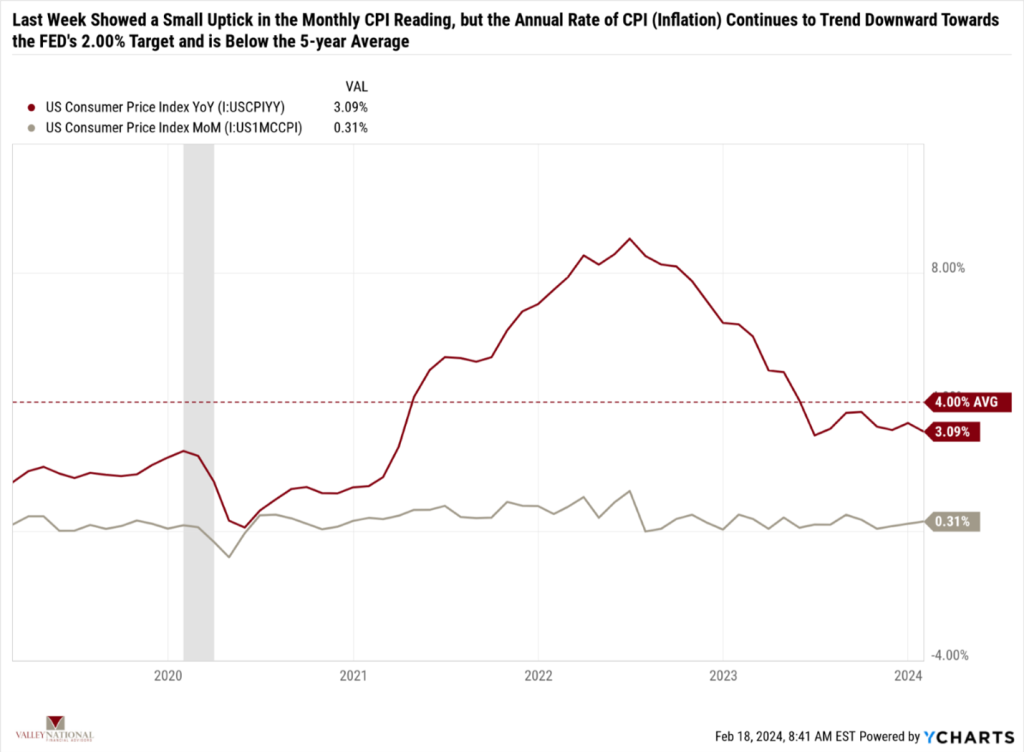

Equity markets sold off, with all three major indexes posting negative returns for the week. (Dow Jones Industrial Average –0.11%, S&P 500 Index –0.42%, NASDAQ –1.34%). Meanwhile, the Russell 2000 Index of small-capitalization stocks rallied +1.17% for the week, breaking from the herd to produce a positive return. Equity markets were pushed into negative territory after releasing January’s CPI (Consumer Price Index) data, which moved higher. The modest move higher in monthly CPI data (+0.31%) reinforces our notion here on The Weekly Commentary that the Fed is data dependent and rate cuts are further off in the future because inflation is not yet tamed in Fed Chairman Jay Powell’s mind. Following the same path, fixed-income markets performed poorly last week, with the 10-year U.S. Treasury bond yield increasing by 13 basis points to 4.30%.

U.S. Economy

As mentioned above, the CPI report for the month of January showed a move higher, but the long-term story remains the same: inflation is coming down. Chart 1 below from Valley National Financial Advisors and Y Charts shows monthly and annual CPI over the past four years. The annual rate of CPI is down from the 9% level we saw in 2022, and the current rate (3.09%) is below the recent average of 4.00%. Monthly figures are more volatile than annual figures, and it is not unusual to see a move higher in monthly CPI in January as that is the month many companies push through higher prices on goods and services. We believe the Fed will not cut interest rates until the second half of 2024, and any moves in interest rates will be predicated by precise data indicating inflation is at or near the Fed’s 2.00% target rate. Equity and fixed-income markets were too quick to price in earlier rate cuts, and markets are simply repricing to reflect that rates are not coming down anytime soon.

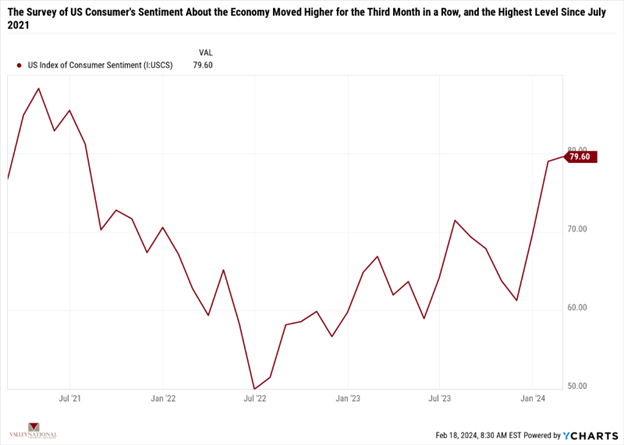

Last week, the University of Michigan released January’s U.S. Index of Consumer Sentiment. Chart 2 below from Valley National Financial Advisors and Y Charts shows the index over the past three years. Since bottoming in July of 2022, the index has moved higher, and more specifically, the last three readings showed improvements in Consumer Sentiment. The index historically indicates increased consumer confidence in economic expansionary periods. Markets understand this, and while we saw a pullback in stocks last week, the trend remains in place – the economy is growing, consumers are spending, and companies are making money.

Policy and Politics

We are in a holiday-shortened week for Washington, with President’s Day on February 19. There are a few important economic reports this week for the same reason. Washington is content on arguing about a funding bill for Ukraine and Israel with or without money for U.S. border controls. It is certainly redundant but necessary to mention that we are in a presidential election year for the U.S. Eventually, that will take center stage in all that happens in Washington, DC.

What to Watch This Week

- U.S. Initial Claims for Unemployment Insurance for the week of Feb 17, released 2/22, prior 218,500.

- U.S. Existing Home Sales for Jan 2024, released 2/17, prior 3.78M.

- U.S. 30-year Fixed Mortgage Rate for the week of Feb 22, released 2/17, prior 6.77%

Summary

Equity markets were early to price in March ‘24 rate cuts, and as the data has unfolded, it is evident that the Fed is not inclined to lower interest rates until the 2.00% inflation target is hit. We are now seeing a repricing in markets to accurately reflect rates cuts much later in 2024 than March. We have said this for a while and stick to our notion of not fighting the Fed. Pushing aside any notion of interest rate cuts, we are still sitting with a growing U.S. economy, especially when compared to other developed nations, which eventually will be good news for equity markets. It is difficult to remain confident about markets when conflicting data exists, but long-term trends remain in place, and our outlook remains cautiously optimistic for 2024. Enjoy the quiet week, and reach out to your advisor at Valley National Financial Advisors for help or questions.