THE NUMBERS

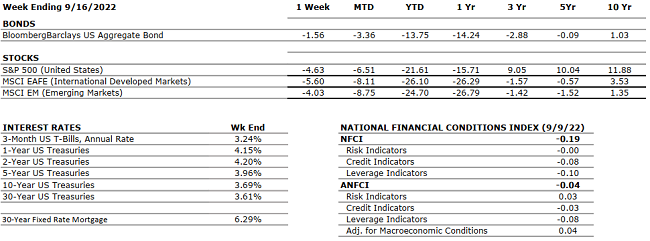

The Sources: Index Returns: Morningstar Workstation. Past performance is no guarantee of future results. Indices are unmanaged and cannot be invested into directly. Three, five and ten year returns are annualized. Interest Rates: Federal Reserve, Mortgage Bankers Association.

MARKET HEAT MAP

The health of the economy is a key driver of long-term returns in the stock market. Below, we assess the key economic conditions that we believe are of particular importance to investors.

|

US ECONOMY |

||

|

CONSUMER HEALTH |

NEUTRAL |

Q1 2022 Real GDP shrunk at a 1.6% annual rate. The main factors that resulted in a decrease in GDP were a surge in imports and trade deficit highlighting that the U.S. is buying more goods from foreign countries. According to the second estimate, real GDP for Q2 2022 decreased at an annual rate of 0.6% (up from the first estimate of -0.9%) marking the second consecutive quarter of declining GDP. |

|

CORPORATE EARNINGS |

NEUTRAL |

The earnings growth rate for Q2 2022 was 6.7% (up from previous estimates of 4.3%) which marked a new post-pandemic low; but still solidly in the “growth” stage. The estimated growth rate for Q3 2022 is 3.2%, which was adjusted downward from 9.8% in June. 6 out of 10 S&P 500 companies that reported earnings beat estimated EPS and 7 beat revenue expectations. |

|

EMPLOYMENT |

NEUTRAL |

U.S. Nonfarm Payrolls for August 2022 increased by 315,000 and the unemployment rate for August rose slightly to 3.7% compared to 3.5% in July. Professional and business services, health care, and retail trade were among the sectors with the most notable job gains. |

|

INFLATION |

NEGATIVE |

The annual inflation rate in the U.S. increased by 8.3% for August 2022 — below the 8.5% in July but above the expected 8.1%. Food prices saw the largest increases since 1979 (11.4%), shelter and used cars also impacted inflation significantly. Core CPI increased 6.3% year-over-year, the most since March, and up from 5.9% in both June and July. |

|

FISCAL POLICY |

NEUTRAL |

Senator Manchin and Majority Leader Schumer reached an agreement on the latest tax and energy bill with incentives for green energy, electric cars, and conversely oil & gas companies for exploration. No changes in private equity taxes or higher tax rates for the very wealthy were enacted. The bill has been officially passed by the Senate. Last week, President Biden announced student loan forgiveness of up to $20,000 subject to income limitations. |

|

MONETARY POLICY |

NEGATIVE |

With inflation still running hot, Fed Chairman Jay Powell is clear on his path to slow the economy enough to cool inflation. The Fed raised rates by 0.75% last week, bringing its target rate to 3.00- 3.25%, and suggesting that additional rate hikes are likely in the coming months. |

|

GLOBAL CONSIDERATIONS |

||

|

GEOPOLITICAL RISKS |

NEGATIVE |

Russia has defaulted on its debt as of late June for the first time since 1918. Sanctions imposed by Western powers effectively isolated Russia and its financial system from Europe and the U.S. making it much harder for Russia to complete international financial transactions. Putin announced last week that Russia is ready to use nuclear weapons to defend its territory as they look to annex four regions in the south and east of Ukraine. |

|

ECONOMIC RISKS |

NEGATIVE |

COVID-19 lockdowns in China are persistent and the ongoing Russian-Ukraine war is causing a major energy crisis in Europe. Putin shut down the pipeline that supplies Europe with natural gas indefinitely until all sanctions affecting Russia are lifted. European countries are struggling to find alternative energy resources and are starting to implement significant restrictions on the use of energy in households and businesses. |

The “Heat Map” is a subjective analysis based upon metrics that VNFA’s investment committee believes are important to financial markets and the economy. The “Heat Map” is designed for informational purposes only and is not intended for use as a basis for investment decisions.